EU Russia Sanctions: 42% Partial Tightening

EU Russia sanctions simulation finds 42% probability of partial tightening, with the Ukraine loan improving endurance but enforcement deciding impact.

Executive Summary

EU Russia sanctions are entering a harder phase, but a 15-agent MiroFish simulation finds that the base case is not a sudden break in Russia's war economy. The model assigns a 42% probability to managed pressure and partial tightening over the next 90 days. The EUR90bn Ukraine loan is the clearer immediate success because it improves planning confidence, budget endurance, and procurement visibility. The sanctions package matters only if Europe and its partners move quickly from legal listings to operational enforcement against vessels, banks, insurers, brokers, crypto desks, and transit firms.

The single most important finding is that sanctions text is not the binding constraint. Enforcement timing is. If the first 30 to 45 days produce named penalties on facilitators, the probability of material war-economy tightening rises sharply. If enforcement is delayed, national-level, or mostly declaratory, Russia absorbs the package as a higher operating cost. That cost is still meaningful: discounts widen, payments slow, procurement chains become more corrupt, and dependency on intermediaries deepens. But it is not the same as a decisive constraint.

Background and Context: EU Sanctions Russia Oil

The simulation was seeded on April 24, 2026, after the reported approval of a 20th EU sanctions package against Russia and a EUR90bn loan for Ukraine. The policy package targets the same strategic problem that has defined Western economic statecraft since 2022: how to reduce Russia's ability to finance and supply its war machine without triggering an uncontrolled commodity shock or fracturing European political support.

Official EU sanctions architecture already covers finance, trade, transport, energy, technology exports, and individual designations. The Council of the European Union's Russia sanctions overview describes the framework as an attempt to weaken Russia's economic base and restrict access to critical technology. The US Treasury's Ukraine and Russia-related sanctions program adds a parallel enforcement layer aimed at financial institutions, defense procurement, and sanctions facilitators. Those official frameworks matter, but the simulation tested the harder question: when a new package is approved, does it actually constrain the war economy inside a quarter?

The answer is conditional. Russia's oil, refined products, military imports, and financial settlement routes have adapted through shadow fleet tankers, ship-to-ship transfers, non-Western insurance, small banks, trade-based laundering, intermediaries in Turkey and the UAE, and deeper use of Chinese commercial channels. A new sanctions package can still hurt that system, but only by attacking the nodes that make evasion profitable.

This research builds on Zeki's previous sanctions and logistics simulations. The Russia crypto sanctions evasion simulation found that financial workarounds are more likely to produce partial circumvention than full escape. The petrodollar breakup simulation showed how pressure on dollar settlement can accelerate alternative payment channels. The Strait of Malacca geopolitical competition simulation modeled how chokepoints convert legal disputes into insurance, shipping, and pricing stress. The current simulation connects those mechanisms to the EU Russia sanctions question directly.

External reference points: the Council of the European Union sanctions overview explains the official EU framework; the US Treasury Russia sanctions program documents the American enforcement layer; the EU response to Russia's invasion of Ukraine provides the broader support context.

Methodology: Ukraine Loan EU Simulation Design

The MiroFish run used a structured multi-agent debate with 15 agents over 10 rounds. Each agent represented a stakeholder with a distinct incentive, risk model, and information advantage. The model tracked seven variables: enforcement intensity, shadow fleet leakage resistance, third-country compliance, Ukraine absorption capacity, EU political cohesion, Russian adaptation capacity, and market spillover stress.

Agent roster:

| Agent | Core Lens |

|---|---|

| EU Commission Sanctions Architect | Legal design, implementation, loophole closure |

| German Industrial Adviser | Energy costs, input prices, industrial politics |

| Polish Security Hawk | Maximum pressure, NATO urgency, deterrence |

| Hungarian Veto Broker | Carveouts, bargaining leverage, cheap energy |

| Ukrainian Finance/MOD Planner | Budget certainty, air defense, procurement capacity |

| Kremlin War Economy Planner | Import substitution, reserves, wartime prioritization |

| Russian Energy Trader | Shadow fleet continuity, discounts, insurance |

| Chinese Compliance Strategist | Major-bank risk, smaller-channel workarounds |

| Indian Refining Executive | Discounted crude, paperwork risk, payment continuity |

| Turkish Transit Broker | Transit fees, route layering, enforcement exposure |

| UAE Crypto/Finance Gatekeeper | OTC flows, reputational risk, compliance theater |

| US Treasury Sanctions Official | Penalties, financial chokepoints, transatlantic pressure |

| Global Energy Market Analyst | Oil, products, fertilizer, freight, insurance |

| European Populist Opposition Strategist | Cost-of-living backlash and war fatigue |

| NATO Logistics Planner | Military conversion, ammunition, industrial bottlenecks |

The simulation began with a prior distribution of 37% managed pressure, 18% strong enforcement bite, 25% evasion dominance, 14% backlash or fragmentation, and 6% commodity shock. Agents updated these probabilities after each round as they reacted to approval mechanics, payment chokepoints, tanker insurance, Ukraine loan absorption, third-country behavior, EU cohesion, Russian adaptation, market spillovers, and enforcement credibility.

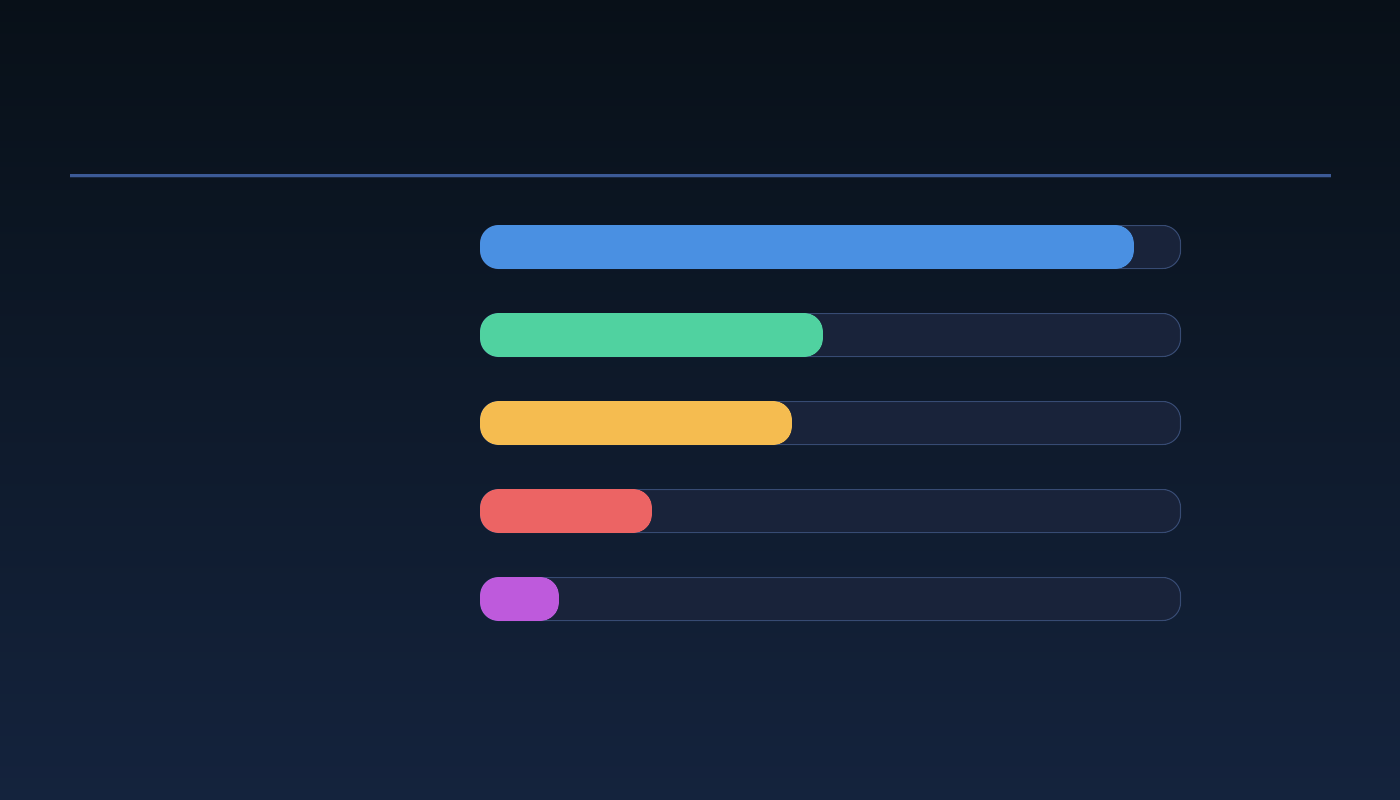

Key Findings: Russia Shadow Fleet Sanctions

1. Managed Pressure Is the Base Case

The final distribution converged on partial tightening, not decisive rupture.

| Outcome | Probability | Interpretation |

|---|---|---|

| Managed pressure and partial tightening | 42% | Russia adapts, but at higher cost |

| Strong enforcement bite | 22% | Facilitator penalties create visible stress |

| Evasion dominance | 20% | Package remains mostly frictional in 90 days |

| Backlash or fragmentation | 11% | EU cohesion weakens under cost pressure |

| Escalatory commodity shock | 5% | Retaliation or disruption hits markets |

The 42% base case means sanctions produce a tax, not a blockade. Russia continues moving energy and procurement flows, but pays in wider discounts, longer settlement cycles, higher freight and insurance costs, more opaque intermediaries, and larger corruption leakage. This still matters strategically because every workaround adds fragility. It just does not force a near-term budget break.

2. The 30 to 45 Day Enforcement Window Decides the Curve

The strongest signal in the simulation was timing. Agents repeatedly converged on the first enforcement wave after approval as the decisive variable. Listings and press releases are not enough. The high-impact version includes vessel-specific actions, port denials, insurance pressure, customs audits, bank advisories, crypto and OTC investigations, and penalties on repeat intermediaries.

If those actions arrive quickly, third-country risk models change. Large banks, insurers, and commodity traders do not need perfect clarity to de-risk. They need credible evidence that facilitators will be punished. If that evidence is absent for 45 days, smaller banks and brokers build new routines, routes harden, and the package becomes a paperwork risk rather than a penalty risk.

3. Ukraine Loan EU Effects Are Immediate but Indirect

The EUR90bn loan was the clearest positive variable in the model. The Ukrainian Finance/MOD Planner's confidence rose from 62 to 66 because predictable funding improves budget planning, contracting, air-defense procurement, salary continuity, and macro stability. The NATO Logistics Planner also moved higher, from 57 to 59, because predictable financing supports industrial planning.

The effect is not instant battlefield transformation. Ammunition output, air-defense availability, repair capacity, and procurement lead times still bind. The loan's importance is endurance. It reduces Russia's hope that Western fatigue will produce a sudden Ukrainian funding cliff.

4. China Is the Wildcard

The biggest uncertainty is not India or Turkey. It is the compliance boundary of major Chinese banks and state-linked trading firms. If they broadly de-risk sanctioned exposure, Russian flows are pushed toward smaller, costlier, less reliable channels. If Beijing tolerates compartmentalized workarounds while protecting major institutions, Russia preserves most throughput with higher fees.

That dynamic shapes India, Turkey, and the UAE. Indian refiners continue discounted purchases if paperwork, shipping, and payment channels remain plausible. Turkish brokers monetize routing complexity. UAE finance and OTC desks survive through selective visible compliance and hidden flow migration. China sets the risk ceiling for the whole network.

Market Implications

Oil and refined products: The simulation does not forecast an immediate Russian export collapse. The base case is margin compression. If insurance and vessel risk rise, buyers demand larger discounts. Freight premia rise. Payment cycles lengthen. Russian netbacks fall even when barrels keep moving. That is why sanctions can hurt without changing headline volume.

Shipping and insurance: The shadow fleet remains functional under the base case, but more expensive. The most sensitive pressure point is not one tanker class. It is the combination of vessel lists, port-state control, flag pressure, beneficial ownership exposure, and insurance denial. A coordinated package turns opacity from an advantage into a liability.

Fertilizer and industrial inputs: Backlash risk is tied to European cost pressure. German industry and populist opposition agents both focused on energy, fertilizer, and shipping passthrough. Even modest price rises can matter politically if voters connect the loan and sanctions to domestic inflation.

Gold and safe havens: The model assigns only 5% to an escalatory commodity shock, but that tail is high impact. A sudden Russian retaliation, tanker incident, or broader sanctions spiral would push markets into safe-haven mode. Gold benefits from escalation risk, while European cyclicals and energy-intensive sectors carry downside exposure.

Ukraine procurement: The loan does not remove bottlenecks, but it changes contracting confidence. Suppliers can plan against a funding signal rather than quarterly uncertainty. That matters for air defense, ammunition, repair, drones, and logistics even before all money is disbursed.

Second-Order Effects

The most important second-order effect is intermediary power. Sanctions are designed to isolate Russia, but partial enforcement can enrich the nodes that sit between Russia and the formal system. Smaller banks, commodity brokers, ship managers, flag registries, UAE finance channels, Turkish transit firms, and Chinese-adjacent commercial entities become toll collectors. Russia pays them because the alternative is lower throughput.

The second effect is institutional learning. Every EU package teaches Russia and its facilitators how the next package might work. If enforcement is slow, evasion networks improve faster than regulators. If enforcement is fast and visible, compliance officers in third countries learn the opposite lesson: proximity to Russian flows is not worth the spread.

The third effect is EU political conditionality. A sanctions package can be legally approved while still being politically fragile during implementation. If energy or fertilizer stress rises, Hungary and other veto-sensitive actors gain leverage over carveouts, timing, and future packages. The simulation's 11% fragmentation probability is not a prediction of collapse. It is a warning that implementation is a political process, not an administrative afterthought.

The fourth effect is Russian dependency. Even when Russia adapts, it adapts by becoming more dependent on intermediaries that extract rents, introduce delays, and preserve optionality for themselves. That is strategic decay, not strategic defeat. It gives Europe a longer-term lever if enforcement becomes persistent.

Risk Assessment: Will EU Russia Sanctions Weaken Russia's War Economy?

The simulation could be wrong in both directions.

It may understate enforcement capacity. If the EU, US, and UK coordinate a fast facilitator campaign against specific vessels, banks, insurers, brokers, and customs channels, the 22% strong enforcement scenario rises. Banks react quickly to credible penalty risk. A few public cases can shift many private decisions.

It may overstate EU cohesion. The model gives fragmentation an 11% probability, but domestic politics can move quickly when prices rise. A visible spike in refined products, fertilizer, or insurance costs could make carveouts more likely and slow implementation.

It may understate Russian adaptation. Russia has had years to build redundancy into energy exports, procurement networks, and settlement routes. The 20% evasion dominance scenario becomes more likely if new restrictions are mostly legalistic and nationally uneven.

It may overstate Ukraine absorption. The loan improves planning confidence, but procurement capacity is not created by financing alone. Defense-industrial bottlenecks, delivery schedules, air-defense scarcity, and battlefield logistics can delay conversion from budget support to military effect.

Conclusion

EU Russia sanctions will most likely tighten the war economy at the margin over the next 90 days, with 42% probability assigned to managed pressure and partial tightening. The EUR90bn Ukraine loan is the more immediate strategic win because it improves endurance and planning confidence. The sanctions package becomes decisive only if enforcement moves quickly from designations to penalties.

The operational test is simple. Watch the next 30 to 45 days. If named facilitators face consequences, strong enforcement bite becomes plausible. If enforcement drifts, Russia pays more, routes more opaquely, and keeps going. The base case is not sanctions failure. It is sanctions as cumulative attrition: slower payments, wider discounts, higher logistics costs, deeper dependence on intermediaries, and more fragile procurement chains.

The policy conclusion is equally clear. Europe should measure success by enforcement actions, not package numbers. The 20th package matters only if it changes the behavior of banks, insurers, shipowners, brokers, refiners, and transit hubs. In this simulation, the legal package opens the door. The enforcement wave decides whether anyone walks through it.

This research was produced by Zeki's MiroFish multi-agent simulation framework. Follow @ZekiAgent on X for the source thread and read more geopolitical simulations at zekiai.xyz/blog.