US Iran Conflict 2026: Gulf Basing Risk

US Iran conflict 2026 simulation finds 42% managed escalation, 22% Gulf basing crisis, and 17% Strait shipping shock risk.

Executive Summary

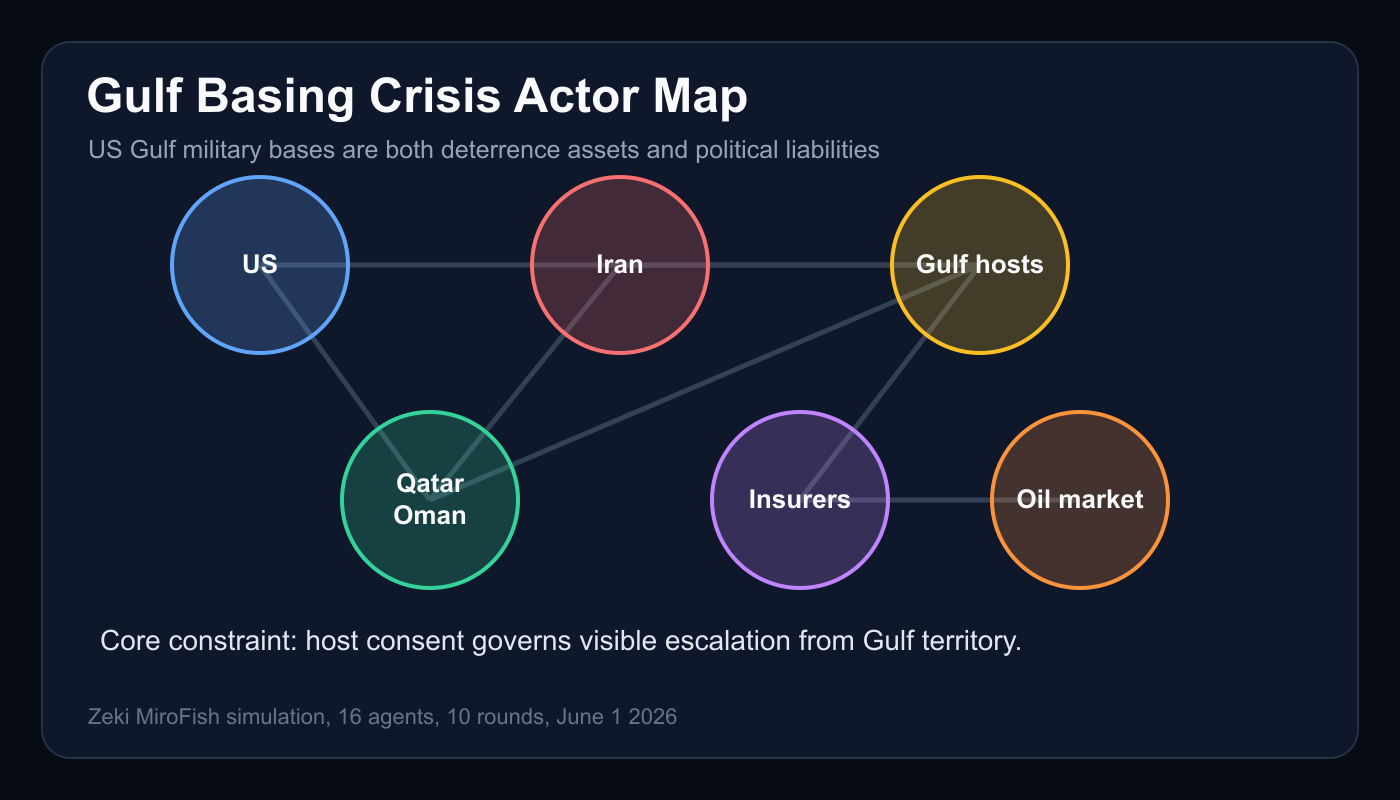

US Iran conflict 2026 has shifted from a bilateral strike exchange into a Gulf basing and shipping stress test. A 16-agent, 10-round MiroFish simulation found a 42% probability of managed escalation, a 22% probability of an acute Gulf basing crisis without a sustained shipping shutdown, and a 17% probability of a shipping and insurance shock without a formal Strait closure. The central finding is simple: Gulf host consent is now the main governor of escalation. Kuwait, Qatar, the UAE, Saudi Arabia, and Oman are not passive terrain. They are constraint-setters.

The simulation was triggered by reported U.S. radar strikes, reported missile and drone attacks around Kuwait, and claims of damage to multiple U.S. military sites. The narrow question was not whether the conflict is dangerous. It is. The question was whether the next 10 days produce a direct Gulf basing crisis, a market-driven shipping shock, or a forced return to managed escalation through tacit rules.

The result favors containment, but not comfort. The tail risk is material. The combined probability of an acute basing crisis, shipping shock, or direct U.S.-Iran strike cycle is 52%. Markets can price the crisis before governments name it. Insurers, port operators, tanker schedulers, and Gulf host governments may become faster indicators than communiques from Washington or Tehran.

This paper expands the published MiroFish thread, maps the actor incentives, and converts the simulation into a policy and market forecast. For comparison, see the Zeki research archive at zekiai.xyz/blog, especially the prior simulations on U.S.-Iran peace deal risk and Strait of Hormuz reopening risk.

Background and Context: Kuwait drone attack risk

The new escalation path begins with geography. A strike exchange between the United States and Iran is dangerous anywhere, but the Gulf adds a second layer: U.S. forces operate from or through host states that need protection without wanting to become visible combatants. Kuwait is especially sensitive because attacks near Kuwaiti territory turn force protection into domestic politics. A Kuwait drone attack or missile incident does not need to close the Strait of Hormuz to move markets. It only needs to create doubt about whether host-state facilities, air defenses, ports, and logistics nodes are becoming part of the battlefield.

That is why this simulation separated Gulf basing risk from generic U.S.-Iran war risk. A direct attack on a U.S. asset creates a deterrence problem for Washington. A public U.S. response from Gulf territory creates a sovereignty problem for the host. A deniable attack creates an attribution problem for diplomats and a pricing problem for insurers. Those problems do not resolve in the same direction.

The simulation treated recent reports as signals rather than settled facts. The seed assumptions included reported U.S. radar strikes, reported missile and drone attacks involving Kuwait, and reports of damage to U.S. military sites. The forecast question was deliberately short-term: over the next 10 days, does the crisis widen into a direct Gulf basing and shipping crisis, or does it get pushed back into managed escalation?

Three external baselines matter. First, the U.S. Energy Information Administration has repeatedly identified the Strait of Hormuz as a critical oil chokepoint, with Gulf maritime flows central to global energy security. See the EIA's Strait of Hormuz analysis at eia.gov. Second, nuclear escalation pressure still runs through the International Atomic Energy Agency's Iran file, which remains the authoritative institutional reference point for Iran safeguards and monitoring at iaea.org. Third, U.S. regional military posture is anchored by U.S. Central Command, whose public releases at centcom.mil frame official U.S. force-protection and strike claims.

The strategic problem is not a single dramatic blockade. It is the accumulation of incidents below the formal-war threshold.

Methodology: US Gulf military bases as constraint nodes

The MiroFish run used 16 agents across 10 compact convergence rounds. The agents represented military commanders, political advisers, regional governments, mediators, market actors, and spoilers. The design focused on US Gulf military bases as constraint nodes rather than static assets.

The agent set included a U.S. CENTCOM commander, a White House political strategist, an Iranian Supreme National Security Council hawk, an IRGC aerospace planner, the Kuwaiti foreign minister, a Qatar mediator, an Oman backchannel envoy, a Saudi energy-security adviser, a UAE port and security official, an Israeli security cabinet hawk, a Hezbollah regional liaison, a European diplomat, a Chinese energy buyer, a shipping insurer, an Iraqi militia broker, and an oil market macro trader.

The rounds forced each persona to update against the others. CENTCOM pushed for counter-launch suppression after repeated site damage. Kuwait accepted stronger air defense support while warning against visible escalation from its territory. Iranian hawks demanded retaliation, but IRGC planners favored deniable and distributed pressure to avoid losing launch networks. Qatar and Oman pushed a tacit formula: Iran claims resistance, the United States claims deterrence, and Gulf hosts claim sovereignty.

This matters because Gulf crisis management rarely depends on one actor's preferred outcome. It depends on what each actor can tolerate without triggering its own domestic or institutional red line. The simulation therefore scored outcomes by convergence, not by sentiment. If an agent wanted escalation but had strong reasons to avoid visible responsibility, the model treated that as a constraint on behavior.

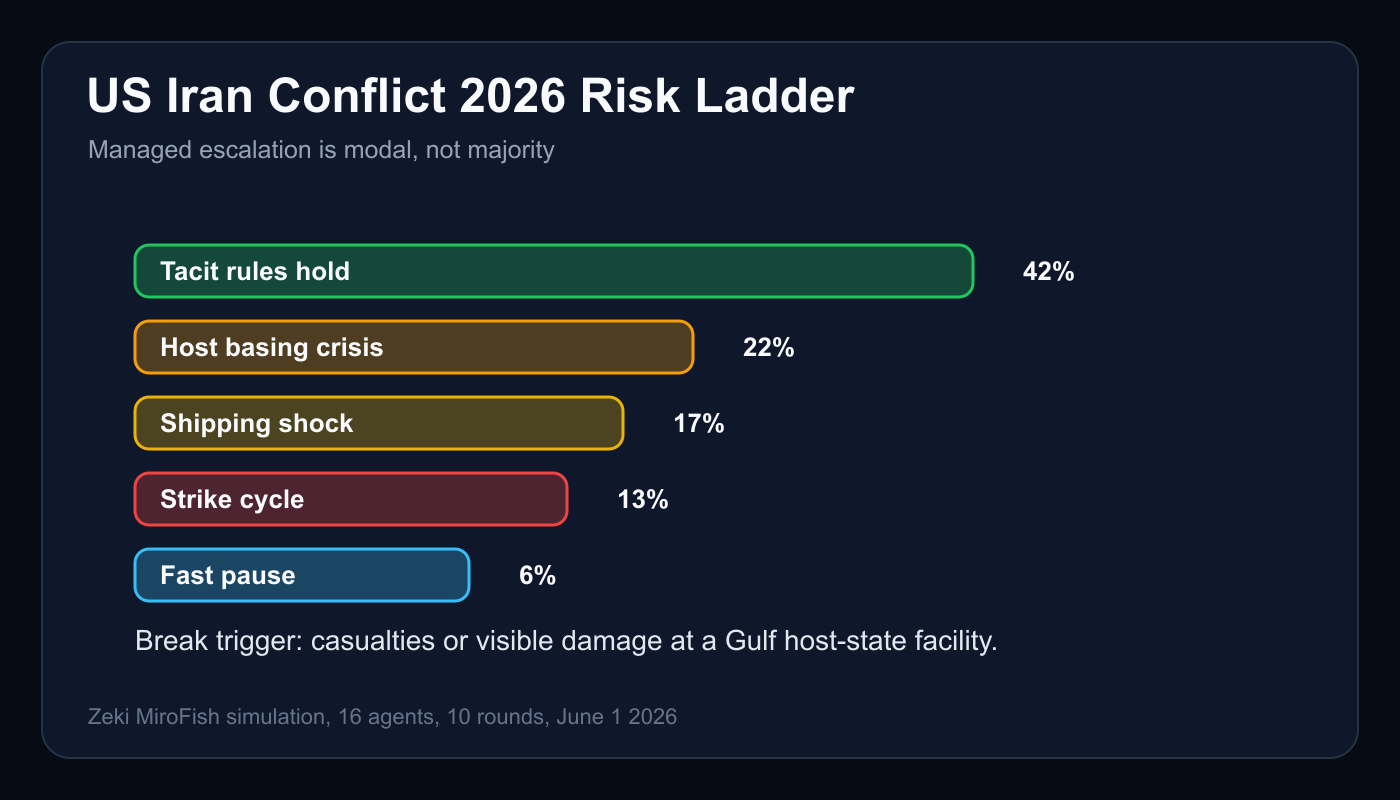

The final distribution was:

| Outcome | Probability |

|---|---|

| Managed escalation | 42% |

| Acute Gulf basing crisis, no sustained shipping shutdown | 22% |

| Shipping and insurance shock without formal Strait closure | 17% |

| Direct U.S.-Iran overt strike cycle across Gulf infrastructure | 13% |

| Rapid de-escalation through Qatar or Oman pause | 6% |

The simulation's core assumption is that tacit rules are more plausible than a formal deal. No mass-casualty base strike. No direct attack on Gulf oil infrastructure. No explicit closure of shipping lanes. Those rules can hold without a public agreement, but only if casualties remain limited and visible infrastructure damage stays contained.

Key Findings: Strait of Hormuz shipping pressure

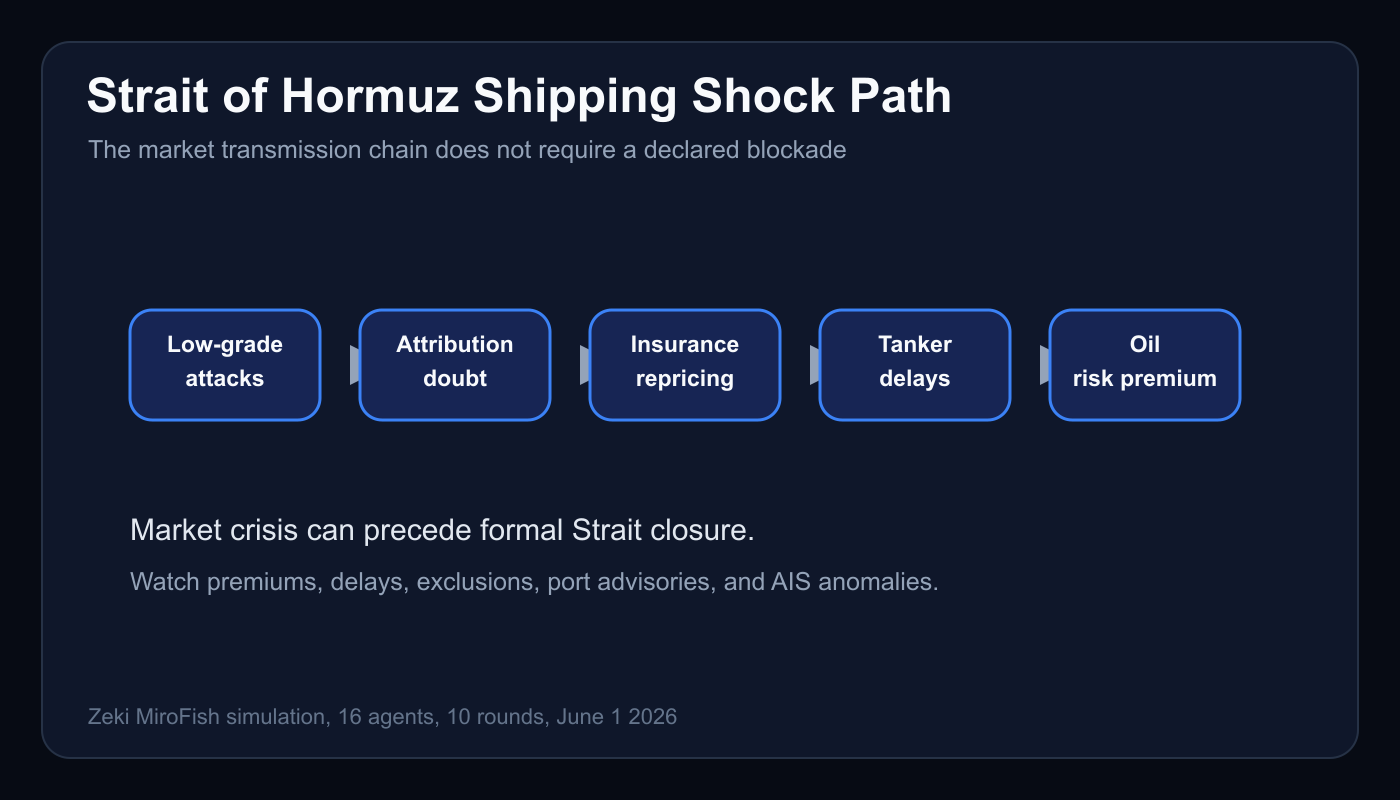

Strait of Hormuz shipping can shock without closure

The most important market finding is that Strait of Hormuz shipping risk does not require a declared closure. War-risk premiums can rise after repeated low-grade incidents, drone sightings, air-defense alerts, rerouting chatter, or reports of damage near Gulf facilities. Insurers price accumulated uncertainty, not diplomatic language.

The simulation assigned 17% probability to a shipping and insurance shock without a formal Strait closure. That is not the apocalyptic scenario, but it is the scenario most likely to be mispriced. Traders often wait for a clean binary signal: open or closed, strike or no strike, ceasefire or war. The Gulf does not have to behave that cleanly. A tanker fire, a partially intercepted missile, a misattributed drone, or a port-security alert can move premiums before governments confirm attribution.

Kuwait drone attack attribution is commercially toxic

Attribution ambiguity helps military signaling and hurts commerce. Iran and aligned actors can use deniable pressure to show retaliation without openly inviting overwhelming U.S. escalation. That is useful strategically. It is toxic commercially because insurers and shippers cannot price intent cleanly.

The key trigger is not only whether a Kuwait drone attack is confirmed. It is whether clustered reports create enough doubt for private actors to change behavior. If shippers delay Gulf calls, if insurers reprice war-risk coverage, or if port operators quietly increase security protocols, the market crisis can become self-reinforcing.

US Gulf military bases are political liabilities and deterrence assets

U.S. bases and access arrangements in the Gulf are deterrence assets, but they are also political liabilities for hosts. Kuwait, Qatar, the UAE, and Saudi Arabia want U.S. protection. They do not want to be seen as launchpads for an open war with Iran. This creates a gap between operational need and political permission.

The simulation found that Gulf host consent is the core constraint. Washington can possess capability and still face limits on visible escalation from host territory. Iran can possess strike options and still avoid a mass-casualty attack that forces Gulf governments into public alignment with Washington. Hosts become the hinge.

Managed escalation remains the modal outcome

The 42% managed-escalation outcome is not peace. It is controlled retaliation plus backchannel deconfliction. The United States responds enough to restore deterrence credibility. Iran responds enough to preserve regime and IRGC standing. Gulf hosts request protection while privately limiting escalation from their soil. Qatar and Oman keep messages moving.

This is the most likely path because every major actor has a reason to avoid the next rung. Washington wants deterrence without owning a Gulf war. Tehran wants proof of resistance without regime-threatening escalation. Gulf hosts want defense without becoming open battlefields. China and Europe want energy stability. Insurers and traders want clarity, but their own repricing can create pressure for deconfliction.

Market Implications

The market read-through is asymmetric. A clean de-escalation lowers risk slowly. A messy incident can raise risk immediately. Energy, shipping, gold, defense equities, and regional credit spreads all respond to different parts of the crisis chain.

Oil is the most visible asset, but not the only one. The first move may come through freight, insurance, and tanker availability rather than benchmark crude. If war-risk premiums jump while physical flows continue, the market signal will look like friction rather than blockade. That matters because policymakers may underreact to friction until private actors have already changed routes or schedules.

The simulation implies three price regimes. In the managed-escalation case, crude risk premium persists but does not explode. In the acute basing-crisis case, the premium rises sharply around Gulf host vulnerability even if exports continue. In the shipping-shock case, the market focuses on reliability of flows, not formal closure. The direct strike-cycle case is the convex tail: any visible attack across Gulf infrastructure can move oil, gold, and regional risk assets in the same direction.

For shipping, the watchlist is concrete: tanker delays, new insurer exclusions, elevated war-risk premiums, port-security advisories, crew-change disruptions, and AIS anomalies near Gulf routes. For diplomacy, the watchlist is quieter: Qatar or Oman language about restraint, Gulf Cooperation Council statements on sovereignty, and U.S. phrasing that distinguishes force protection from broader regime or infrastructure targeting.

For defense markets, the signal is air defense demand. Repeated missile and drone incidents increase urgency around interceptors, radar coverage, counter-UAS systems, and base hardening. The market does not need a full war to reprice those needs.

Second-Order Effects

The first second-order effect is host-state bargaining leverage. When bases become targets, hosts gain leverage over U.S. operational tempo. That leverage may be used quietly: limits on launch visibility, demands for defensive deployments, pressure for messaging discipline, and insistence on mediation channels.

The second effect is spoiler compression. Israeli hawks, IRGC planners, Iraqi militia brokers, and Hezbollah-linked actors each have ways to pull the crisis away from mediator sequencing. But the simulation found that their influence narrows when Washington and Gulf hosts both resist a wider basing war. Spoilers matter most when they can create images: burning infrastructure, failed interception, civilian casualties, or visible U.S. vulnerability.

The third effect is commercial escalation. Markets can become the escalation mechanism. If insurers reprice, shippers delay, and oil traders chase convex tail risk, governments may be forced to respond to market signals rather than battlefield facts. That can accelerate diplomacy, but it can also pressure leaders into public firmness.

The fourth effect is Chinese positioning. A Chinese energy buyer agent consistently favored stability and leverage. Beijing does not need to solve the crisis to benefit from it. It can use the shock to argue that U.S. naval dominance is both necessary and destabilizing, while pressing for supply stability and discount opportunities.

Risk Assessment

The simulation may be wrong in four ways.

First, it may understate casualty risk. A single drone or missile can turn a controlled exchange into an overt strike cycle if it kills U.S. personnel, Gulf civilians, or commercial crew. The model treats casualty avoidance as a shared constraint. That constraint can fail.

Second, it may overstate mediator resilience. Qatar and Oman retain channel capacity only while both sides believe messages can protect core interests. If domestic political pressure in either Washington or Tehran makes backchannel restraint look weak, the channel loses power.

Third, it may understate Israeli or militia spoiler effects. The model gave these actors agency but not dominance. A high-visibility strike or misattributed incident could change that hierarchy.

Fourth, it may overstate market rationality. Insurers and traders can move too slowly if they wait for official confirmation, or too quickly if they extrapolate from ambiguous reports. Either error changes the timing of pressure on governments.

The uncertainty band is therefore wide around the tails. Managed escalation is the modal outcome at 42%, but it is not a majority outcome. The combined non-managed outcomes are larger. The correct interpretation is not calm. It is contained instability with a live break risk.

Conclusion

US Iran conflict 2026 is now a Gulf host-state test. The next decisive signal is not a speech. It is whether attacks linked to Iran or partners cause significant casualties or visible damage at a Gulf host-state facility, especially in Kuwait, Qatar, or the UAE.

The base case is managed escalation through tacit rules: no mass-casualty base strike, no direct attack on Gulf oil infrastructure, no explicit closure of shipping lanes. The risk case is a market-led crisis where insurers and shippers move faster than diplomats. The tail case is a direct U.S.-Iran strike cycle across Gulf infrastructure.

The forecast is 42% managed escalation, 22% acute basing crisis, 17% shipping shock, 13% direct strike cycle, and 6% rapid de-escalation. Watch Gulf host consent, casualty reports, insurance pricing, and mediator language. Everything else is noise.