China Russia Energy: Alignment Risk Model

China Russia energy simulation finds 62% odds of managed alignment, 18% hard bloc risk, and sanctions risk centered on Chinese banks.

Executive Summary

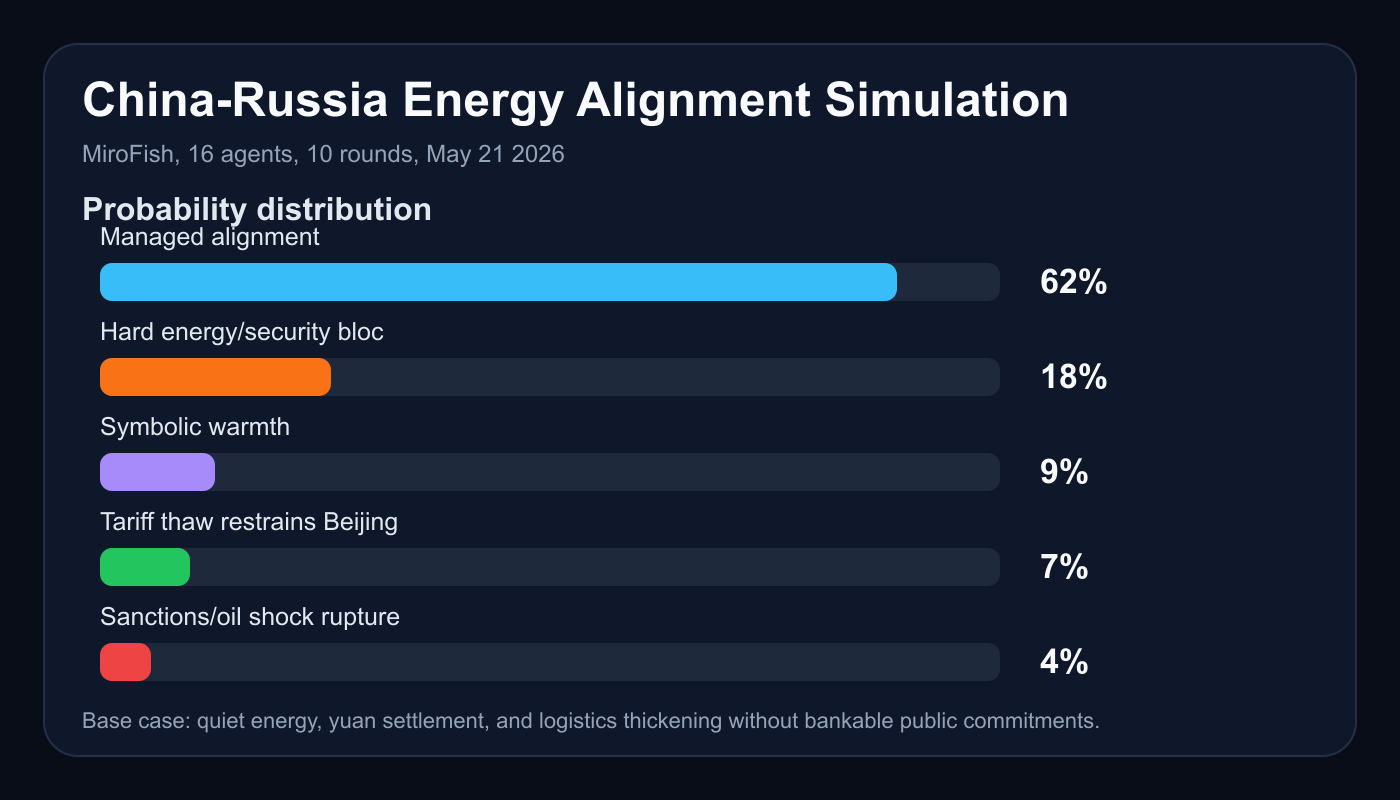

China Russia energy is the central variable in the post-summit triangle between Xi Jinping, Vladimir Putin, and Donald Trump. A 16-agent, 10-round MiroFish simulation of the Xi-Putin Beijing summit after Trump-Xi talks assigns 62% probability to managed alignment: quiet energy, yuan settlement, discounted commodities, and logistics workarounds without a public hard commitment that would endanger the US-China tariff thaw. The hard energy and security bloc outcome sits at 18%. The key finding is that Beijing wants Russian leverage, not Russian dependency risk on its balance sheet.

The strongest hedge signal is what did not appear: a bankable public breakthrough on a major pipeline package such as Power of Siberia 2. Summit rhetoric can be warm while contract risk remains cold. Putin needs durable Chinese demand, capital, and proof that Russia is not isolated. Xi wants cheap supply, strategic optionality, and anti-US signaling, but Chinese banks and export manufacturers still carry the penalty if Washington and Europe move from rhetoric to secondary sanctions.

The simulation does not say the relationship is weak. It says the relationship is asymmetric. Russia is the more urgent seller. China is the more disciplined buyer. That gap turns the summit from a bloc-formation event into a pricing, compliance, and optionality event.

Background and Context: China Russia Trade After the Summit

The May 20 Beijing meeting took place in a narrow strategic window. Xi hosted Putin after visible signals of a possible US-China tariff thaw, while oil-market stress and sanctions fatigue created pressure on Western enforcement. The public language around the meeting emphasized friendship, multipolar order, energy cooperation, and the durability of the China-Russia relationship. Those themes are real, but they are not sufficient to prove a binding energy-security alignment.

The policy question is more specific: does Beijing convert warmth into enforceable commitments, or does it keep Russia close while staying below the threshold that triggers a US or EU backlash? That distinction matters because China can deepen cooperation through channels that are hard to headline but easy to measure later: yuan settlement, shipping insurance workarounds, discounted crude, machinery flows, bank routing, and a slow expansion of bilateral logistics.

The simulation used the latest public signals recorded in the seed document, including reports that the summit was heavy on friendship language but did not deliver a visible major pipeline deal. It also modeled the effect of tariff politics. If Washington wants a China trade headline, it has an incentive to tolerate ambiguity as long as Beijing avoids a public Russia package that humiliates the thaw.

For context, the same site has tracked adjacent geopolitical cascade risks in prior simulations, including the Trump pauses Iran strike Gulf risk model, the Gaza flotilla sanctions risk model, and the US-Iran nuclear deal simulation. The common pattern is institutional friction. Leaders announce intent. Banks, ministries, markets, and allies decide how much of it becomes operational reality.

Authoritative reference points for the channels in this model include the Kremlin public record, China's Ministry of Foreign Affairs, the US Trade Representative's China country page, and the US Treasury's OFAC sanctions framework. Energy-market stress is best read alongside official statistical sources such as the US Energy Information Administration and market policy updates from the International Energy Agency.

Methodology: 16-Agent MiroFish Simulation

The simulation asked one question over a 60-day horizon: does the Xi-Putin summit produce hard energy and security alignment that undercuts the tentative US-China trade thaw, or does Beijing keep Russia close while avoiding commitments that would trigger US and EU backlash?

MiroFish ran 16 agents through 10 rounds. The agent set covered state principals, energy planners, sanctions enforcers, banks, exporters, and regional market actors. Personas included Xi Jinping, Vladimir Putin, Donald Trump, a Chinese NDRC energy planner, a Chinese major bank risk officer, the Russian energy minister, a Russian finance technocrat, the US Trade Representative, a US Treasury sanctions official, Ukraine's presidential office, the UK Foreign Office, an EU sanctions coordinator, an Indian refinery executive, a Gulf energy minister, a Chinese export manufacturer, and a NATO eastern-flank security adviser.

The model weighted ten variables: Power of Siberia 2 progress, tariff thaw incentives, Russian capital needs, Ukraine sanctions cohesion, Chinese secondary-sanctions risk, Iran-linked oil shock, nationalist optics, European enforcement, India-Turkey-Gulf arbitrage, and Trump political incentives. Agents were not asked to predict the most dramatic story. They were asked to bargain under constraints.

The output is a probability distribution, not a claim of certainty. The value is in identifying which constraint moves first. In this run, the constraint was not presidential warmth. It was Chinese financial exposure.

Key Findings: Power of Siberia 2 Is the Signal, Not the Slogan

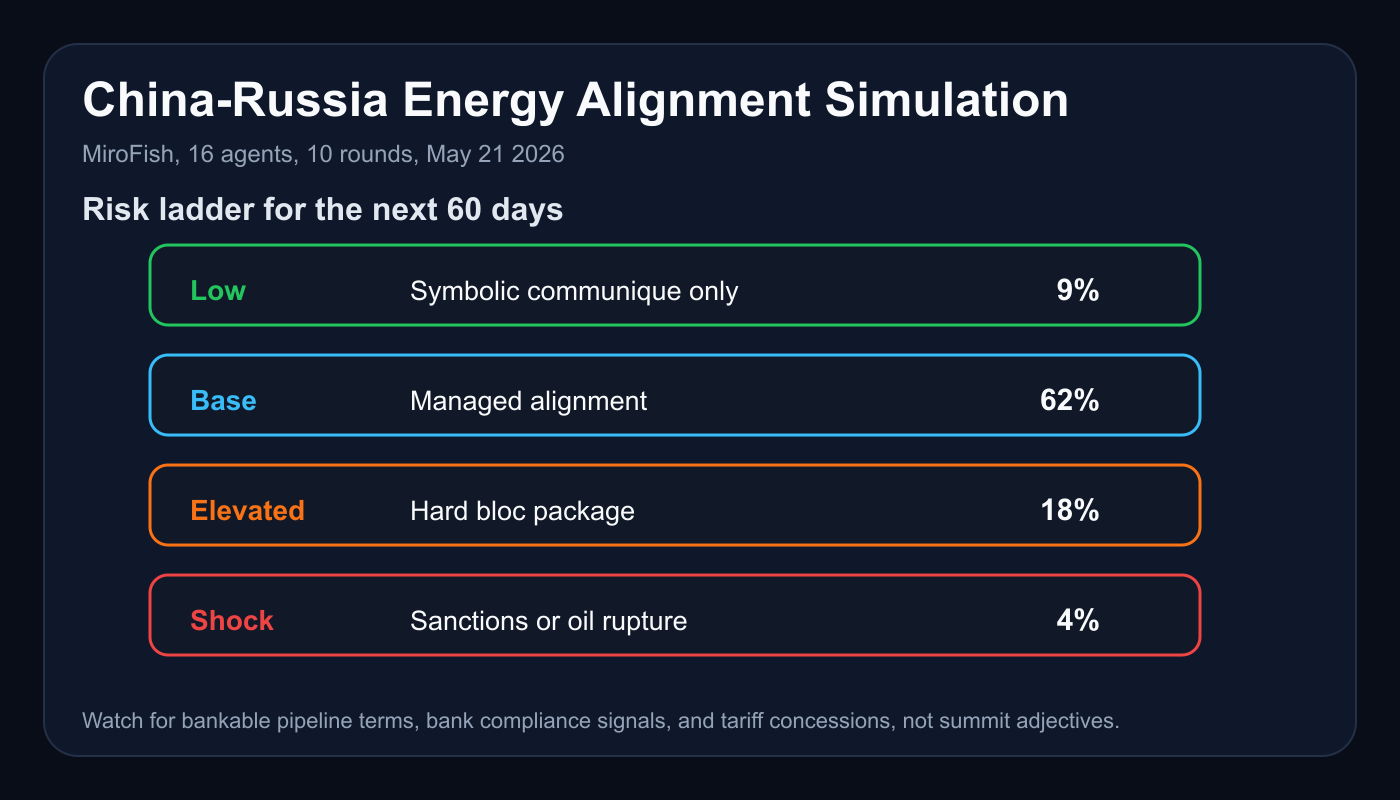

The final distribution was clear:

| Outcome | Probability |

|---|---|

| Managed alignment: quiet energy and yuan channels, no public hard commitments | 62% |

| Hard energy and security alignment undercutting the US-China thaw | 18% |

| Mostly symbolic warmth with limited material change | 9% |

| US-China tariff thaw dominates and restrains Beijing | 7% |

| Sanctions or oil shock rupture forces sharper bloc dynamics | 4% |

The most important finding is that Power of Siberia 2 functions as a market test. General statements about energy cooperation are cheap. A bankable, priced, financed, and scheduled pipeline commitment is not. If Beijing wants to lock in Russian supply without accepting Russia's stranded infrastructure risk, it will keep language constructive and terms vague.

That is exactly why the absence of a major public pipeline package matters. It leaves China with leverage. Russia remains dependent on a buyer that can demand discounts. China gets strategic depth without taking a visible step that would allow Washington, Brussels, or London to build a clean sanctions case.

China Russia Trade Thickens Below the Headline

The base case is not stasis. The simulation expects quiet thickening in China Russia trade, especially where enforcement is difficult and incentives are aligned. Yuan settlement can expand. Discounted Russian crude and refined products can continue moving through complex routes. Machinery and components can flow in categories that are hard to police without broad economic costs.

This is the uncomfortable middle path for Western policy. It produces real strategic support for Moscow without the clean public trigger that makes allied enforcement easy. A summit communique may not change the market. A sequence of bank routing decisions, refinery contracts, and shipping workarounds can.

US China Tariff Thaw Limits Beijing's Appetite for Visibility

The tariff thaw is a ceiling on public alignment. Trump wants visible trade wins, agricultural purchases, tariff relief optics, and lower fuel prices. Beijing wants reduced friction for exporters and manufacturers. Those incentives do not eliminate China-Russia cooperation. They push it into forms that preserve deniability.

The simulation's 7% outcome where the tariff thaw fully restrains Beijing is small because strategic rivalry with the United States still gives China a reason to keep Russia close. But the tariff thaw is large enough to discipline optics. China can help Russia in ways that do not look like an alliance treaty. That is the modal path.

Chinese Banks Are the Veto Players

The single most important factor was China's secondary-sanctions risk tolerance among major banks and export-linked firms. Xi can set strategic direction, but large Chinese financial institutions price dollar-clearing risk, correspondent banking risk, and balance-sheet exposure. Export manufacturers care about US and European demand. Their incentives are not identical to Russia's.

This makes hard alignment difficult. A public package that ties Chinese banks to sanctioned Russian energy infrastructure would concentrate risk. Quiet settlement channels distribute risk. Distributed risk is harder to punish and easier for Beijing to adjust.

Market Implications: Energy, Shipping, Gold, and Sanctions Risk

The market implication is not a single oil-price call. It is a regime map. Managed alignment means Russian supply remains available, China keeps buying, and enforcement leakage persists. That can cap some upside in crude by preventing a clean supply break, while keeping a sanctions-risk premium alive in freight, insurance, and compliance-sensitive trade finance.

For oil, the key variable is whether Iran-linked supply stress raises the political cost of strict Russia enforcement. If crude prices rise sharply, the United States, Europe, India, Gulf states, and China all gain incentives to prioritize supply stability over sanctions purity. That does not remove sanctions. It makes enforcement selective.

For shipping and insurance, managed alignment raises complexity rather than immediate crisis probability. More transactions may route through less transparent chains. That benefits intermediaries and arbitrage buyers but increases compliance volatility. A single designation, port incident, insurance refusal, or payment blockage can ripple faster than the underlying energy flow changes.

For gold and safe-haven assets, the hard-bloc outcome is the more important tail. At 18%, it is not the base case, but it is large enough to monitor. A visible energy-security package would intensify bloc framing, raise sanctions expectations, and push investors toward geopolitical hedges. The 4% sanctions or oil shock rupture outcome is smaller, but it carries the highest market convexity because it combines enforcement escalation with supply fear.

For Russia, managed alignment is financially useful but strategically disappointing. Moscow gets buyers and optics. It does not get the guarantee it wants. If commitments stay vague, Russia remains a price-taker selling into Chinese leverage.

For China, managed alignment is the efficient frontier. It preserves access to cheap energy, keeps Russia from collapsing into isolation, and avoids writing a sanctions invitation in public.

Second-Order Effects: Quiet Alignment Beats Bloc Theater

The first second-order effect is dependence inversion. Publicly, China and Russia can describe the relationship as equal and strategic. Economically, the bargaining asymmetry grows if Russia needs China more than China needs one specific Russian project. That gives Beijing a stronger hand on price, timing, financing, and public language.

The second effect is sanctions ambiguity. Western governments prefer clean target sets. Managed alignment denies them that. If support moves through trade categories, bank subsidiaries, shipping intermediaries, and third-country arbitrage, enforcement becomes a political choice rather than a mechanical trigger.

The third effect is alliance fatigue. Ukraine, NATO's eastern flank, the UK, and the EU have incentives to call out China-Russia alignment. But if oil prices are high, European cohesion weakens. The simulation found that energy-price politics can make sanctions enforcement appear principled in speeches and partial in practice.

The fourth effect is US messaging discipline. If Trump can claim tariff progress, farm purchases, or reduced pressure on American consumers, Washington may downplay ambiguous China-Russia cooperation. That creates a zone where Beijing can deepen practical ties while avoiding spectacle.

The fifth effect is India, Turkey, and Gulf arbitrage. These actors do not need to choose a bloc to shape outcomes. Their refining, routing, financing, and pricing decisions determine how much Russian energy pressure leaks around formal sanctions architecture.

Risk Assessment: What Could Break the Model

The model could be wrong in three main ways.

First, Power of Siberia 2 or a similar package could move faster than public reporting indicates. If a bankable agreement emerges with financing, pricing, construction terms, and political guarantees, the hard-alignment probability rises immediately. The simulation treats missing public detail as a hedge signal. Hidden detail would change the input.

Second, a sharper oil shock could force governments into less coherent behavior. The model assigns only 4% to a sanctions or oil shock rupture that forces sharper bloc dynamics. That probability is low because many actors prefer ambiguity. It is not zero because oil shocks compress decision time and reward actors that already have workaround channels.

Third, Washington or Brussels could decide to make an example of a Chinese institution. The model assumes China wants to avoid that and the West wants to preserve some room for trade and price stability. A deliberate enforcement strike against a major Chinese bank, insurer, or energy intermediary would change Beijing's calculus. It could deter further alignment, or it could push China toward open confrontation if leaders decide the penalty is unavoidable.

The uncertainty band is widest around political visibility. Quiet cooperation is easier to sustain than public commitment. The more Xi and Putin need domestic theater, the more they risk making the relationship easier to sanction. The more Washington needs a trade win, the more it may tolerate ambiguous cooperation that would otherwise invite escalation.

Conclusion

The next 60 days should be measured by contracts, banks, and shipping flows, not summit adjectives. The MiroFish base case is 62% managed alignment: China keeps Russia close, absorbs cheap energy, expands yuan and logistics channels, and avoids a public hard package that threatens the US-China tariff thaw. The hard-bloc scenario is real at 18%, but it requires Beijing to accept more visible sanctions risk than the current incentives justify.

The actionable takeaway is simple. Watch Power of Siberia 2 terms, Chinese bank compliance behavior, tariff-thaw deliverables, Russian discounting, and oil-price stress. If pipeline detail appears and Chinese banks stay relaxed, the bloc risk rises. If communiques stay warm while financing stays vague, managed alignment remains the correct read.

Russia gets optics. China gets optionality. Markets should price the difference.