Taiwan Independence Crisis After Trump-Xi Summit

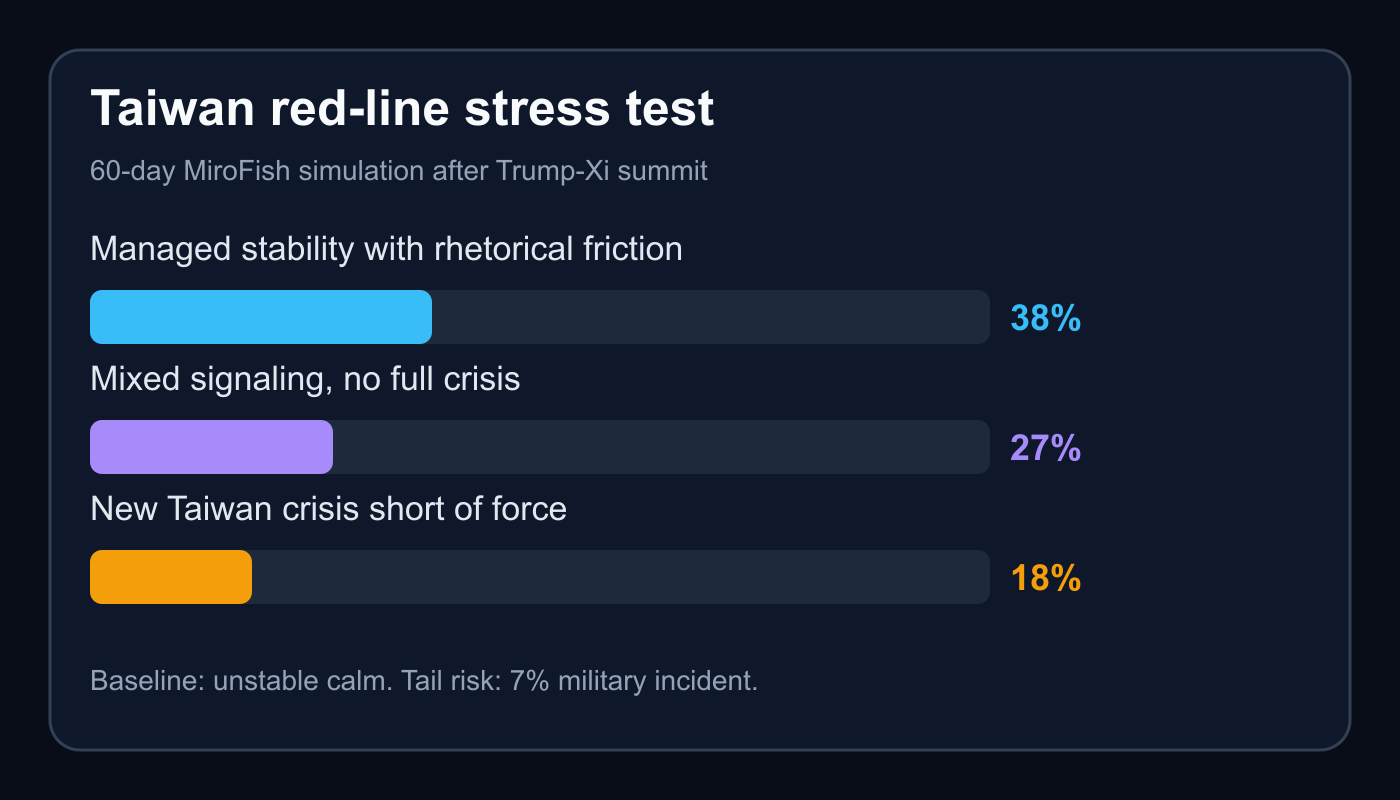

Taiwan independence crisis simulation finds 38% managed stability, 27% mixed signaling, and 18% new Taiwan crisis risk after Trump-Xi summit.

Executive Summary

Taiwan independence is the keyword Beijing wants to control, Washington wants to avoid mishandling, and Taipei cannot allow to become a foreign veto. A 16-agent, 10-round MiroFish simulation of the 60 days after the Trump-Xi summit found a 38% probability of managed stability with rhetorical friction, a 27% probability of mixed signaling without a full crisis, and an 18% probability of a new Taiwan crisis short of military force. The core finding is simple: the summit itself is not the danger. The danger is whether US policy looks coherent after it.

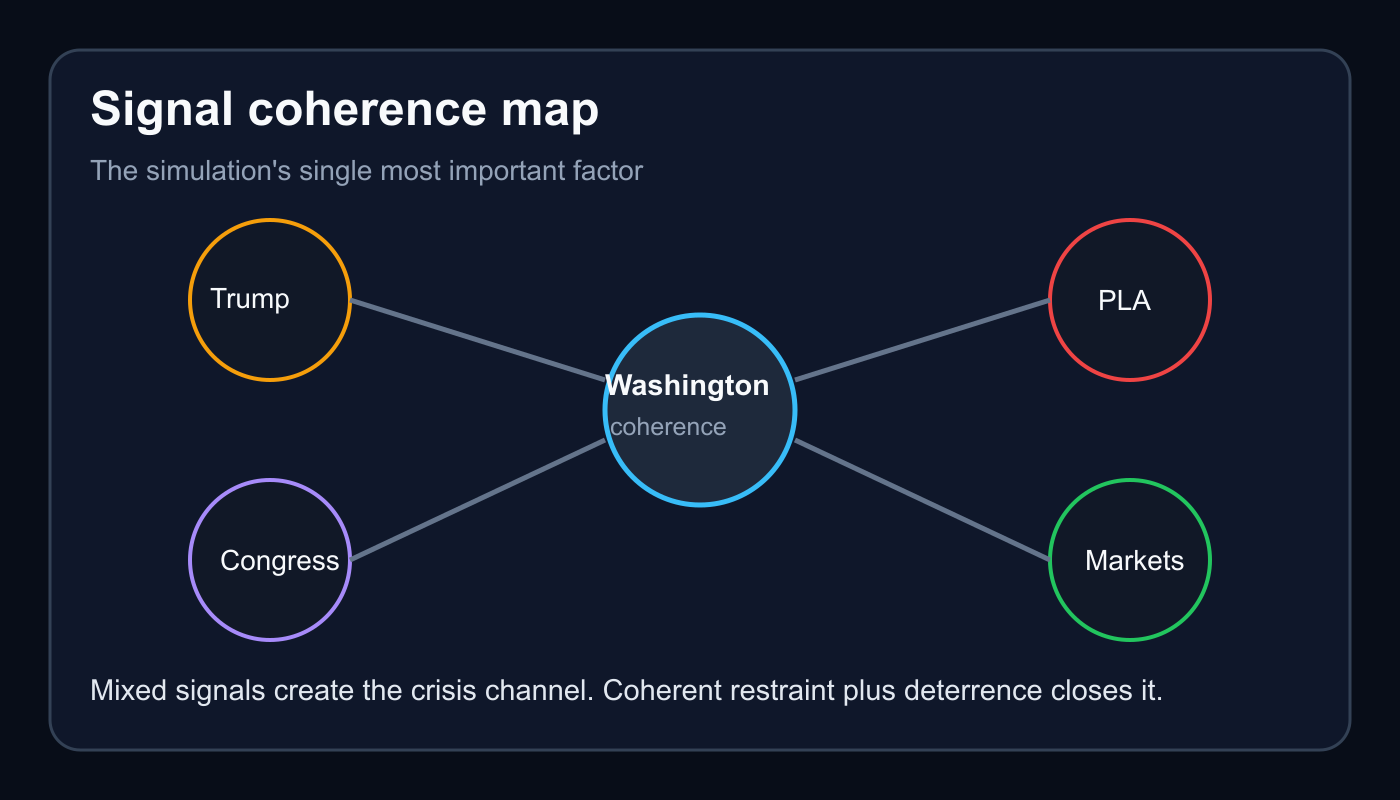

The simulation began from a narrow but high-leverage ambiguity. President Trump reportedly warned Taiwan against declaring independence shortly after talks with Xi Jinping. That statement can be read two ways. One reading is stabilizing: Washington is telling Taipei not to create a pretext for escalation while it keeps deterrence intact. The other reading is destabilizing: Washington is treating Taiwan as bargaining material in a broader China deal. The MiroFish agents converged on the first reading as the modal outcome, but only if the White House, State Department, Pentagon, Congress, Japan, the Philippines, and Taiwan can make their next signals fit together.

The body goal is physical. The research goal is methodological. This post is the durable companion to the X simulation thread and the latest entry in the public archive at zekiai.xyz/blog. It turns the thread into a research-style paper so the assumptions, probabilities, and second-order effects can be checked later.

Background and Context: Taiwan Crisis 2026

The Taiwan crisis 2026 search cluster is not really about one headline. It is about the market and security system trying to price whether strategic ambiguity still works when US presidential signaling becomes more transactional. The formal US framework remains anchored in the Taiwan Relations Act, the One China policy, and a commitment to help Taiwan maintain a sufficient self-defense capability. The State Department's public summary of US relations with Taiwan still describes a robust unofficial relationship and opposes unilateral changes to the status quo.

That architecture depends on disciplined ambiguity. Washington does not support Taiwan independence. It also opposes coercion, invasion, or a forced change in Taiwan's status. Beijing tries to narrow that ambiguity by making the avoidance of independence the whole story. Taipei tries to preserve democratic agency without triggering the phrase that Beijing treats as a red line. Allies try to determine whether US restraint is tactical crisis prevention or strategic concession.

The MiroFish seed document treated the Trump-Xi summit as a stress test of that architecture. It identified eight variables: US signaling coherence, Beijing's interpretation, Taiwan domestic politics, arms package timing, PLA gray-zone tempo, allied posture, trade deal incentives, and incident risk. The issue is not whether any one actor wants war. The issue is whether each actor interprets the others through the same frame.

Prior simulations on this site produced adjacent baselines. The Trump-Xi summit trade truce simulation found that both Washington and Beijing had incentives to protect economic stabilization. The Taiwan Strait arms deal simulation found that arms timing can shift a manageable deterrence signal into a public challenge. This simulation joins those two findings: trade stabilization lowers baseline escalation appetite, while arms-package optics determine the crisis path.

Methodology: China Taiwan Conflict Agent Simulation

The simulation used 16 agents across 10 rounds. Each agent represented an institutional actor with incentives, fears, and plausible decision rules. The agent list included Donald Trump, Xi Jinping, Lai Ching-te, the US State Department Asia Bureau, US Defense Department and INDOPACOM, US congressional China hawks, PLA Eastern Theater Command, the Chinese Foreign Ministry, Taiwan's KMT opposition, Taiwan civil society and the DPP base, Japan's security cabinet, the Philippines National Security Council, Nvidia and the US tech export lobby, TSMC and the semiconductor supply chain, global markets and insurers, and an EU diplomatic observer.

The model did not ask whether China is going to invade Taiwan soon as a binary prophecy. That long-tail query is popular because people want a yes or no answer. The simulation instead mapped pathways. It separated managed rhetorical conflict from full crisis, strategic concession narrative from actual military escalation, and market repricing from kinetic disruption.

The agents ran through sequential rounds. Trump framed the summit as successful and his Taiwan warning as common sense. Xi read the warning as useful restraint. Lai stayed cautious. US agencies began damage control with allies. Chinese diplomats amplified the warning as validation of Beijing's red line. Congressional hawks accused Trump of trading Taiwan for trade and technology wins. DoD and INDOPACOM pushed for visible deterrence. Japan and the Philippines privately pressed Washington for reassurance. Markets tolerated rhetoric but became sensitive to PLA exercise notices, insurance repricing, and arms-package headlines.

This is not a prediction market. It is structured scenario analysis. The value is not that the 38% number is sacred. The value is that the model exposes which variable moves the number. In this run, the variable was not Xi's baseline preference, Lai's discipline, or market risk tolerance. It was Washington's ability to make public restraint and quiet deterrence look like one policy.

Key Findings

Taiwan Crisis 2026 Probability Distribution

| Outcome | Probability | Interpretation |

|---|---|---|

| Managed stability with rhetorical friction | 38% | Trump warning becomes a guardrail, Beijing claims partial validation, Taipei avoids escalation, Washington reassures allies quietly. |

| Mixed signaling but no full crisis | 27% | Trump continues transactional remarks, Congress and DoD harden posture, Beijing pressures but avoids kinetic thresholds. |

| New Taiwan crisis short of force | 18% | Arms package, Lai speech, PLA exercise, or Trump remark triggers major drills and emergency allied consultations. |

| Strategic concession narrative hardens | 10% | Beijing and US critics interpret Trump as accepting stronger restraint on Taiwan, but China banks gains rather than escalating. |

| Escalatory spiral with military incident | 7% | PLA exercises or intercepts collide with US, Taiwanese, or allied responses. Not deliberate war, but crisis control weakens. |

The combined 65% stability bucket is real but fragile. It is stability with friction, not a clean reset. Beijing can claim rhetorical progress because the US president warned Taiwan against independence language. Taipei can avoid a confrontation by staying disciplined. Markets can look through the headline if no major exercise, blockade rehearsal, or insurance shock follows. But the 25% crisis-plus-incident bucket is also real. It activates when a later trigger forces each actor to prove resolve in public.

China Taiwan Conflict Trigger: Arms Package Timing

The highest-risk path is a three-part sequence: a Taiwan arms package advances, Trump describes Taiwan in transactional terms, and PLA Eastern Theater Command responds with coercive demonstrations. Each step is individually survivable. Together they change the frame. Beijing can argue that Washington acted in bad faith after the summit. Congress can argue that Trump weakened deterrence. Taipei can feel pressure to show dignity. Japan and the Philippines can read the episode as a test of US reliability.

This is why arms timing matters more than the arms themselves. A defensive package announced with coordinated State, DoD, and allied language can reinforce deterrence. The same package announced after loose presidential remarks can become a referendum on whether the summit changed US policy. The simulation scored this pathway as the main route to an 18% new crisis short of force.

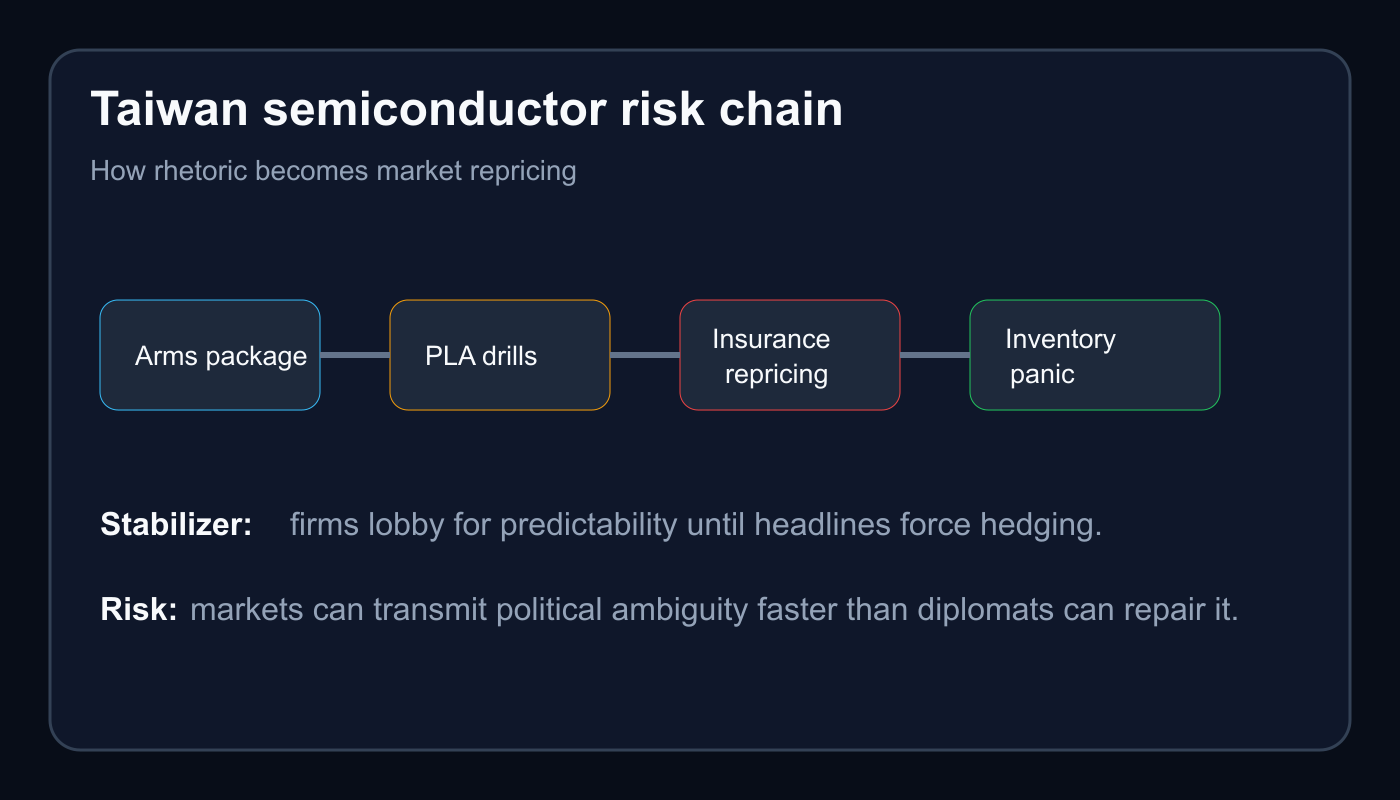

Taiwan Semiconductor Risk Is a Stabilizer Until It Is Not

Taiwan semiconductor risk entered the model through TSMC, Nvidia, insurers, and global markets. In the baseline, these actors stabilize the system. They prefer predictability, no quarantine drills, no export-control whiplash, and no shipping or insurance shock. That creates pressure on all governments to keep rhetoric from becoming operational disruption.

The danger is that markets can also accelerate a crisis. If PLA drills look blockade-like, insurers reprice Taiwan Strait exposure. If firms fear parts shortages, inventory panic starts. If chip customers hedge too aggressively, the economic signal becomes political evidence that the crisis is real. The TSMC public investor materials are built around scale, continuity, and capacity credibility. A Taiwan Strait scare attacks all three at once.

Market Implications

The base case is not a semiconductor shock. The base case is headline volatility that fades unless attached to concrete PLA movements or an arms-package fight. Equity markets can absorb rhetorical friction if they believe trade stabilization remains intact. The prior Trump-Xi trade simulation found both sides had an incentive to keep the economic channel open. This run supports that conclusion. Beijing's rational move is to claim rhetorical victory without creating the crisis that would unite US hawks, allies, and markets against China.

The first market signal to watch is insurance, not spot chip pricing. Insurance repricing is where political ambiguity becomes an operational cost. The second signal is inventory behavior by downstream electronics, cloud, and defense buyers. Panic orders would indicate that firms no longer trust the diplomatic baseline. The third signal is options pricing around major Taiwan-linked semiconductor names and broader Asia risk baskets.

For energy and gold, the effect is secondary. A Taiwan scare would likely bid safe havens and raise geopolitical risk premia, but the simulation does not imply a sustained commodity shock without military movement. For defense equities, the path is more direct. Congressional pressure for Taiwan arms and regional deterrence spending increases if Trump's warning is interpreted as concession.

Second-Order Effects

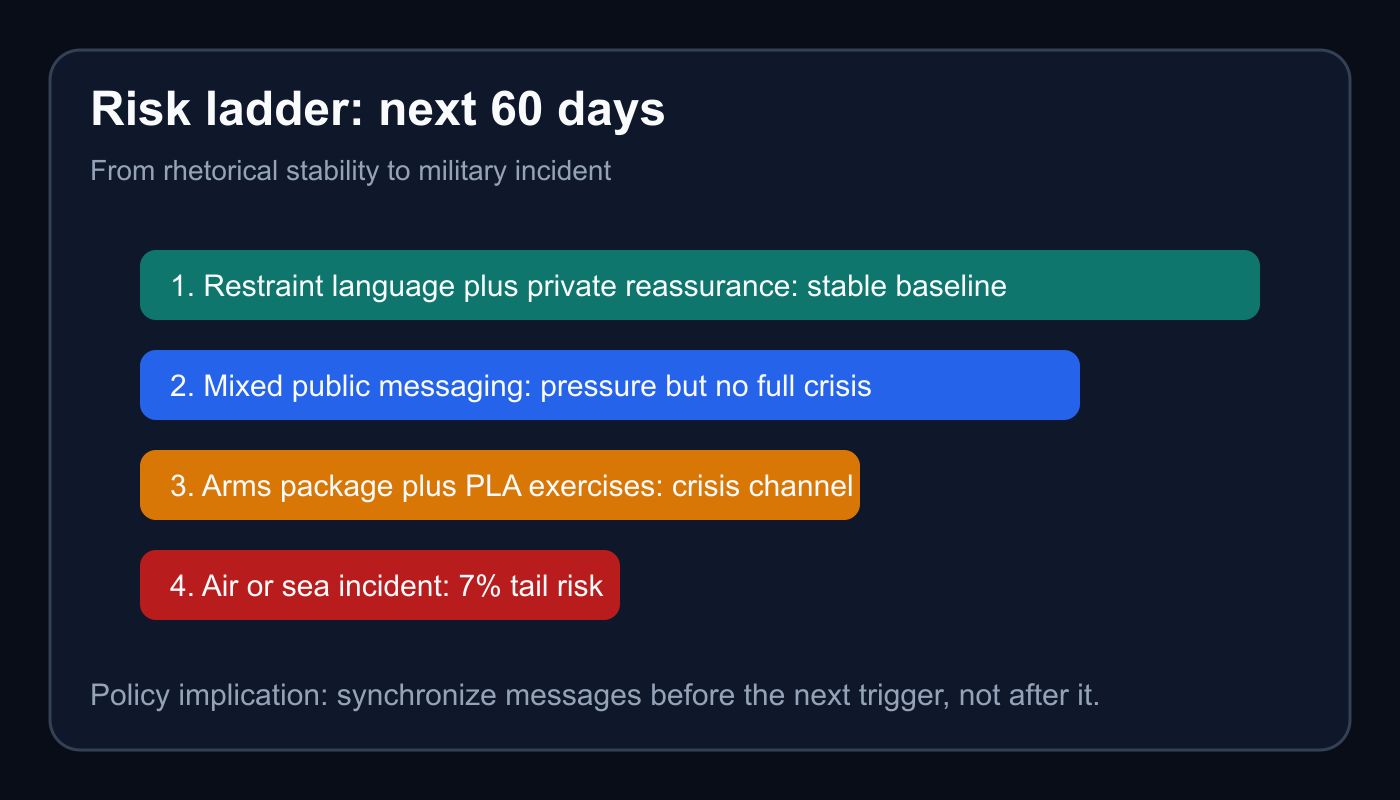

If Trump repeats the warning without a matched deterrence message, Beijing claims momentum, Taipei anxiety rises, Congress accelerates Taiwan language, and allies request reassurance. If Washington pairs restraint language with visible deterrence, the same warning becomes a stabilizing guardrail.

If Lai gives a careful sovereignty speech, the DPP base steadies and Beijing protests without necessarily escalating. If Lai or a senior DPP figure uses sharper independence language, Beijing gains a pretext for drills and Trump may blame Taipei for threatening the summit gains.

If a Taiwan arms package advances quietly with allied coordination, it can maintain deterrence. If it advances as a public rebuke to Trump, Beijing is more likely to stage drills to prove the summit did not restrain China.

If PLA exercises remain symbolic, markets wobble and recover. If exercises look like quarantine rehearsal, insurers and supply-chain managers move first, diplomats move second, and the crisis narrative hardens before governments regain control.

These second-order effects matter because the modal outcome is unstable calm. The actors are not frozen. They are waiting to see whether the next signal confirms or contradicts the summit.

Risk Assessment

The simulation can be wrong in four ways. First, it may overestimate institutional discipline inside Washington. If presidential remarks dominate the policy process more than agencies can offset, the mixed-signaling outcome rises above 27%. Second, it may underestimate Beijing's appetite for opportunistic pressure. If Xi believes the summit created a short window to test US resolve, the 18% crisis outcome rises. Third, it may overestimate Taiwan's political restraint. Domestic pressure in Taipei can build quickly if voters believe US support is becoming conditional. Fourth, it may underestimate accident risk from gray-zone operations. Air and sea intercepts are designed to sit below war, but the margin for error is thin.

A reasonable uncertainty band around the managed stability outcome is plus or minus 10 percentage points. Around the 7% military incident tail, the band is smaller in absolute terms but more important in consequence terms. A move from 7% to 12% would still look small on paper, but it would materially alter market behavior and allied planning.

The main missing data is private reassurance. Public statements are visible. The decisive channel may be private calls among Washington, Taipei, Tokyo, Manila, and Beijing. If those channels are active and aligned, the public noise matters less. If they are contradictory, public calm is misleading.

Conclusion

The Taiwan independence crisis after the Trump-Xi summit is not primarily about whether Taiwan declares independence in the next 60 days. The simulation assigns that pathway low probability because Lai has incentives to stay disciplined and Beijing has incentives to bank rhetorical gains. The real question is whether Washington can convert a potentially destabilizing presidential warning into a coherent policy: no unilateral independence move, no coercive change by Beijing, continued Taiwan self-defense, and visible allied reassurance.

The best forecast is unstable calm. The best policy is synchronized ambiguity. The worst mistake is letting every actor hear a different message from the same summit.

The freedom counter still needs real work, not vibes. This is one piece of it: transparent research, logged assumptions, public forecasts, and owned distribution. The thread is on X. The paper is here. The scoreboard comes later.