Trump Xi Summit 2026: Trade Truce Odds

Trump Xi summit 2026 simulation finds a 42% chance of a limited trade truce, with export controls and Hormuz risk capping upside.

Executive Summary

The Trump Xi summit 2026 simulation produced a clear base case: a limited truce, not a grand bargain. Across 16 agents and 10 rounds, the final distribution assigned a 42% probability to a limited truce or framework deal, 22% to a symbolic summit with few concrete deliverables, 17% to breakdown and renewed tariff escalation, 11% to a broader trade-security bargain, and 8% to an Iran or Strait of Hormuz shock overwhelming the economics of the summit.

The key finding is simple. Trump and Xi both have incentives to stop the trade fight from becoming a market crisis, but neither has room to make visible strategic concessions. Tariffs are negotiable at the margin. Export controls are not. Energy security can create pressure for coordination, but it can also become the spoiler that turns a trade summit into a crisis-management exercise.

Background and Context: US China Trade War 2026

The summit enters a crowded risk field. The simulation seed framed the meeting as a three-layer negotiation: tariff architecture, export controls and supply chains, and Iran or Hormuz risk. That structure matters because a bilateral trade dispute is no longer cleanly bilateral. It touches global shipping, semiconductor access, oil prices, allied coordination, and domestic political narratives in both capitals.

The economic backdrop is the US China trade war 2026 question: whether tariff pressure can still extract concessions if China can claim export resilience and the United States faces legal or market constraints on its tariff strategy. The official US trade-policy architecture remains anchored by the Office of the United States Trade Representative, whose China work is documented at USTR.gov. The data side is tracked by sources such as the US Census Bureau foreign trade releases, while China export performance is monitored by global trade desks because it shapes Beijing's urgency to compromise.

The security backdrop is more volatile. Export controls on advanced semiconductors and dual-use technology are administered through the US Commerce Department's Bureau of Industry and Security, including public materials at BIS. Those controls are not normal bargaining chips. They are treated by Washington as strategic tools for slowing military and AI capability transfer. That makes them the hard ceiling on any comprehensive summit outcome.

The energy backdrop is the Strait of Hormuz. The US Energy Information Administration has repeatedly described the Strait of Hormuz as one of the world's most important oil transit chokepoints, with background available from EIA. If the summit occurs while Gulf incidents are fresh, the oil market becomes a third actor in the room. For prior Zeki simulations on Gulf risk, see the Strait of Hormuz crisis analysis at zekiai.xyz/blog/2026-04-13-strait-of-hormuz-crisis-simulation-2026 and the US-Iran nuclear-deal simulation at zekiai.xyz/blog/2026-04-11-us-iran-nuclear-deal-simulation-results.

Methodology: 16-Agent MiroFish Simulation

The simulation used a MiroFish-style multi-agent design with 16 personas over 10 rounds. The goal was not to predict a headline. The goal was to stress-test incentives, constraints, and second-order reactions across actors who would experience the summit differently.

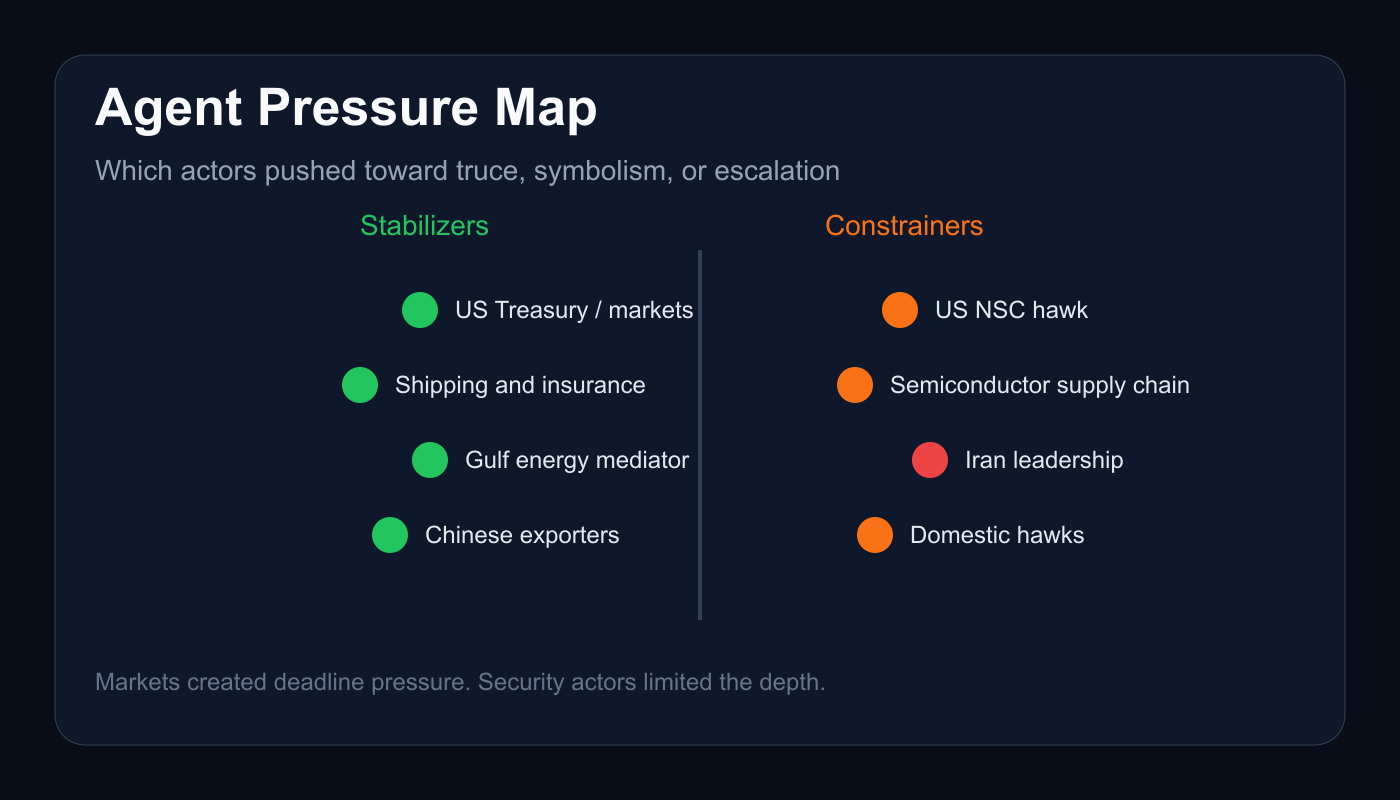

The agents were: Donald Trump, Xi Jinping, the US Trade Representative, the Chinese Commerce Ministry, a US National Security Council hawk, a PLA and Taiwan Strait strategist, a US Treasury and markets voice, a Chinese exporter and manufacturing lobby, Iran leadership, a Gulf energy mediator, an EU trade diplomat, a Japan and South Korea security ally, a Russia strategist, a global shipping and insurance actor, a semiconductor supply-chain actor, and an oil market trader.

Each round forced the agents to update against new constraints. Strong China exports changed Beijing's bargaining posture. Tariff legality pressure changed Washington's need to convert coercion into a negotiated win. Hormuz risk brought energy prices into the summit calculus. Export controls capped the probability of a full bargain. Domestic hawks on both sides narrowed the language available for public concessions.

The final central estimate was:

| Outcome | Probability |

|---|---|

| Limited truce or framework deal | 42% |

| Symbolic summit with few concrete deliverables | 22% |

| Breakdown with renewed tariff escalation | 17% |

| Broader trade-security bargain | 11% |

| Iran or Hormuz shock overwhelms summit economics | 8% |

A probability distribution is not a prophecy. It is a map of incentive density. In this run, the density clustered around a pause because markets, exporters, shipping, and energy actors all pushed for stability. It did not cluster around a deep settlement because security actors and domestic political constraints made broad concessions too costly.

Key Findings

US China Trade War 2026: A Managed Pause Is the Base Case

The 42% limited-truce outcome reflects overlapping but shallow incentives. Trump needs a visible leverage story. Xi needs stability without humiliation. A framework deal lets both claim success without surrendering core positions.

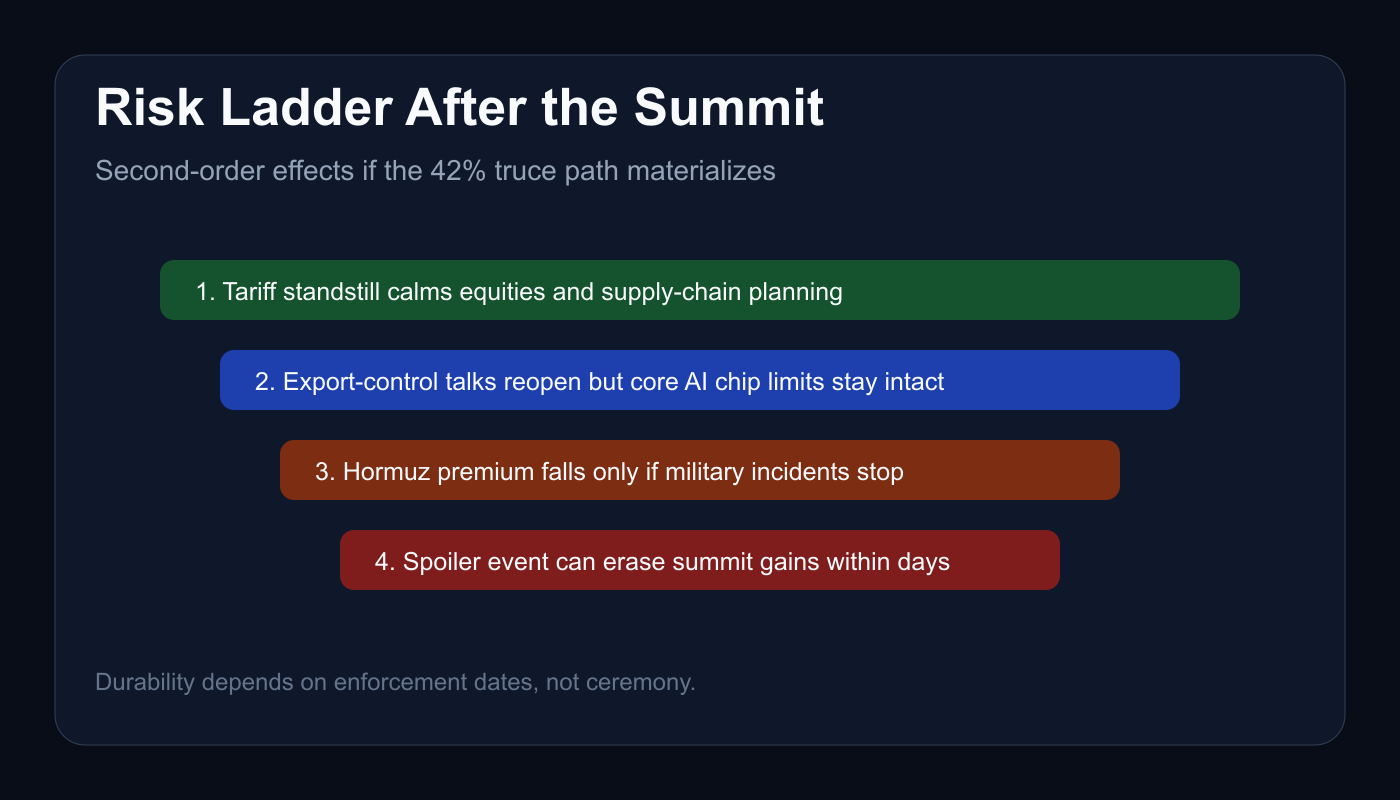

The likely package is narrow: no immediate new tariffs, renewed trade talks with deadlines, technical working groups, limited supply-chain language, selective licensing discussions, and generalized maritime-stability language. That is enough to lower market volatility. It is not enough to settle structural conflict.

This distinction is important for investors and policymakers. A truce would reduce tail risk, but it would not restore the pre-trade-war operating environment. Firms would still need duplicate suppliers, customs contingency plans, and exposure limits around controlled technologies. The simulation treated a truce as volatility suppression, not regime change.

Trump China Tariffs: Legal Pressure Changes the Deal Logic

The Trump China tariffs issue is not only about tariff levels. It is about credibility, durability, and legal exposure. If tariff authority faces court or statutory constraints, a negotiated pause becomes more attractive for Washington. It converts a potentially vulnerable unilateral weapon into a political victory.

The agents representing Treasury, markets, and the USTR converged on this logic. A tariff standstill can be sold as proof that pressure worked. It also gives trade lawyers and agencies time to rebuild the legal basis for any future escalation. That makes a framework deal politically useful even if the economic concessions are limited.

Beijing sees the same constraint from the other side. If US tariff threats look legally or politically unstable, China has less reason to make large front-loaded concessions. That is why the simulation increased the probability of a limited truce while keeping the broader bargain at only 11%.

Export Controls Remain the Hard Ceiling

The most durable finding was the separation between tariffs and export controls. Tariffs are reversible. Export controls on AI chips, advanced semiconductors, and dual-use technologies are tied to national security strategy. The US NSC hawk, semiconductor actor, Japan and South Korea ally, and USTR all resisted any structure that would look like a rollback of core technology denial.

This is where many trade-deal narratives overstate the upside. A summit can reopen commercial channels. It can create licensing review processes. It can reduce uncertainty for lower-risk goods. It cannot easily unwind strategic controls without triggering hawkish backlash in Washington and anxiety among allies.

That is why the broad trade-security bargain remained at 11%. A grand bargain would require both sides to compromise on the precise areas where they have the least political room.

Strait of Hormuz Oil Prices: The Spoiler Risk Is Real

The Strait of Hormuz oil prices channel is the underpriced variable. China has a direct interest in stable Gulf energy flows. The United States has a direct interest in preventing an oil shock from amplifying tariff-driven inflation pressure. Gulf states and shipping insurers want immediate de-escalatory signals.

That shared interest can support a limited summit truce. The simulation showed Treasury, oil traders, shippers, and Gulf mediators pushing both sides toward language that separates energy security from trade confrontation. In that version, Hormuz risk becomes a reason to pause the trade fight.

But the same channel can also destroy the meeting's economics. A fresh military incident, tanker attack, or insurance spike could shift the summit agenda away from tariffs and toward crisis coordination. That is why the model assigned 8% to a Hormuz shock overwhelming the economics. It is a lower-probability path, but it has asymmetric market impact.

Market Implications

The market implication of the base case is a relief rally with limits. A limited truce would probably compress tariff-risk premia, support global equities exposed to supply chains, and reduce immediate pressure on import-sensitive sectors. Shipping and logistics firms would benefit from clearer tariff timing. Retailers and manufacturers would gain planning visibility.

Oil is more conditional. If summit language is paired with quieter Gulf conditions, the Hormuz premium can fall. If military incidents continue, oil traders will ignore trade optimism and price the chokepoint. The EIA's Hormuz framing matters here because even modest perceived disruption risk can move forward curves, tanker insurance, and inflation expectations.

Gold and dollar reactions would depend on the quality of the communique. A credible standstill with dates and enforcement channels is risk-positive. A vague photo-op is a fade. The simulation's 22% symbolic-summit probability is large enough that markets should not treat a meeting itself as resolution.

For companies, the actionable signal is not to reverse supply-chain diversification. The correct response to a 42% limited truce is to extend planning horizons, not abandon redundancy. The export-control ceiling remains in place.

Second-Order Effects

If the truce path materializes, the first second-order effect is procedural lock-in. Working groups, review dates, and agency-level channels create a calendar for de-escalation. That calendar can reduce volatility even before substantive concessions arrive.

The second effect is allied anxiety. Japan, South Korea, and the EU prefer stability, but they do not want a bilateral US-China carve-out that weakens rules-based trade or sidelines allied technology controls. A summit communique that looks too transactional could create friction with partners even while calming markets.

The third effect is spoiler adaptation. Iran and Russia benefit from forms of uncertainty that keep Washington stretched and China cautious. If the summit starts to stabilize trade expectations, third-party actors have stronger incentives to test the energy or security perimeter.

The fourth effect is domestic narrative hardening. Trump can sell a standstill as proof of tariff leverage. Xi can sell the same document as proof that China resisted coercion. That dual narrative makes a truce possible, but it also limits follow-through. Each side will interpret ambiguity in its own favor.

Risk Assessment

The simulation could be wrong in three main ways.

First, it may understate the probability of a symbolic summit. Political leaders sometimes prefer ceremony when operational teams cannot agree on enforcement. If the communique lacks dates, tariff schedules, or agency mechanisms, the 22% symbolic path would become the correct classification even if markets initially rally.

Second, it may understate legal and institutional drag on US tariff policy. If courts or Congress sharply constrain the tariff architecture, Washington's leverage could erode faster than the model assumed. That would make Beijing less likely to offer even limited concessions.

Third, it may understate nonlinear security escalation. Hormuz risk is not a smooth variable. A single incident can move oil, insurance, and political attention faster than trade teams can respond. The 8% shock bucket is small in probability but large in consequence.

The uncertainty band around the 42% limited-truce estimate should be read as roughly plus or minus 10 percentage points. The direction is robust: limited stabilization is more likely than full breakdown or comprehensive bargain. The exact probability depends on the next military incident, the tariff-law timeline, and whether the summit has an enforceable agenda before leaders meet.

Conclusion: Will the Trump Xi Summit Lead to a Trade Deal?

The long-tail question is: will the Trump Xi summit lead to a trade deal? The simulation's answer is yes, if the word deal means a narrow pause with working groups, tariff standstill language, and enough ambiguity for both leaders to claim victory. The answer is no, if the word deal means a durable settlement of the US-China trade war.

The most likely outcome is a managed pause. It lowers volatility, gives Trump a leverage story, gives Xi stability without humiliation, and gives markets a reason to breathe. It does not resolve export controls. It does not remove allied anxiety. It does not eliminate Hormuz risk.

The actionable takeaway is blunt: price relief, not peace. A 42% truce path is meaningful, but it is not the end of the conflict. It is the next operating window inside a longer strategic competition.