US Brazil Critical Minerals: Trump-Lula Deal Odds

US Brazil critical minerals deal odds: a 16-agent simulation finds 36% chance of a limited tariff pause and non-exclusive minerals framework.

Executive Summary

US Brazil critical minerals cooperation is likely to move forward as a narrow, autonomy-preserving bargain rather than a grand realignment. A 16-agent, 10-round MiroFish simulation assigns a 36% probability to the central outcome: a limited practical package by June 30, 2026, combining a tariff pause, non-exclusive minerals framework, financing discussions, and selective security cooperation. The most important finding is simple: the deal works only if Washington accepts that Brazil will not choose the United States over China in public.

The simulation gives a 28% probability to managed friction, where the leaders produce a cordial communique but no meaningful deliverables. A broader strategic bargain receives only 10%. The median outcome is therefore not failure, but disciplined modesty. Trump can claim a hemispheric supply-chain win. Lula can claim balanced diplomacy. US investors can begin due diligence. China can monitor without immediate retaliation.

The single deal-killer is messaging. If Trump frames the meeting as Brazil bending under tariff pressure or joining an anti-China bloc, Lula's domestic coalition and Itamaraty have strong incentives to slow-walk or dilute the framework. If the language stays modular, practical, and non-exclusive, the bargain survives.

Background and Context: Trump Lula Meeting and Brazil Critical Minerals

The May 7, 2026 Trump-Lula White House meeting sits at the intersection of trade pressure, hemispheric security, and supply-chain diversification. The immediate agenda is tactical: avoid tariff escalation, identify practical economic cooperation, and keep the relationship from becoming another theater of ideological conflict. The deeper agenda is strategic: Brazil has mineral resources, agricultural leverage, industrial capacity, and a diplomatic identity built around autonomy. The United States wants less dependence on Chinese-controlled supply chains. Those two facts create both the bridge and the trap.

Critical minerals have become a policy category because clean energy, defense systems, electronics, grid hardware, electric vehicles, and advanced manufacturing all depend on inputs that are geographically concentrated. The US Geological Survey maintains the US critical minerals list. The International Energy Agency tracks how mineral demand is tied to energy security. The US Department of Energy has also treated critical materials as an industrial policy priority.

Brazil is relevant because it can offer scale without fitting neatly into a US-China binary. It is a major commodity exporter, a BRICS member, a country with deep China trade ties, and a Western Hemisphere democracy with reasons to welcome capital, processing capacity, and infrastructure finance. That combination is valuable precisely because it is not a clean alignment story.

Trade tension is the near-term constraint. Searches around "US Brazil tariffs" and "Trump Lula meeting" show that public interest clusters around tariffs, meeting timing, and whether the relationship can produce tangible outcomes. Searches around "Brazil critical minerals" and "US Brazil critical minerals agreement" point to a more specialized but higher-value policy audience: investors, trade lawyers, mining firms, industrial-policy officials, and geopolitical analysts.

This post extends the simulation research line at zekiai.xyz/blog, including prior work on supply-chain chokepoints, tariff bargaining, and crisis escalation. The question here is narrower than whether Brazil becomes an American minerals proxy. It does not. The question is whether a practical package can be designed so both leaders benefit without forcing Brazil to abandon strategic autonomy.

Methodology: US Brazil Critical Minerals Simulation Design

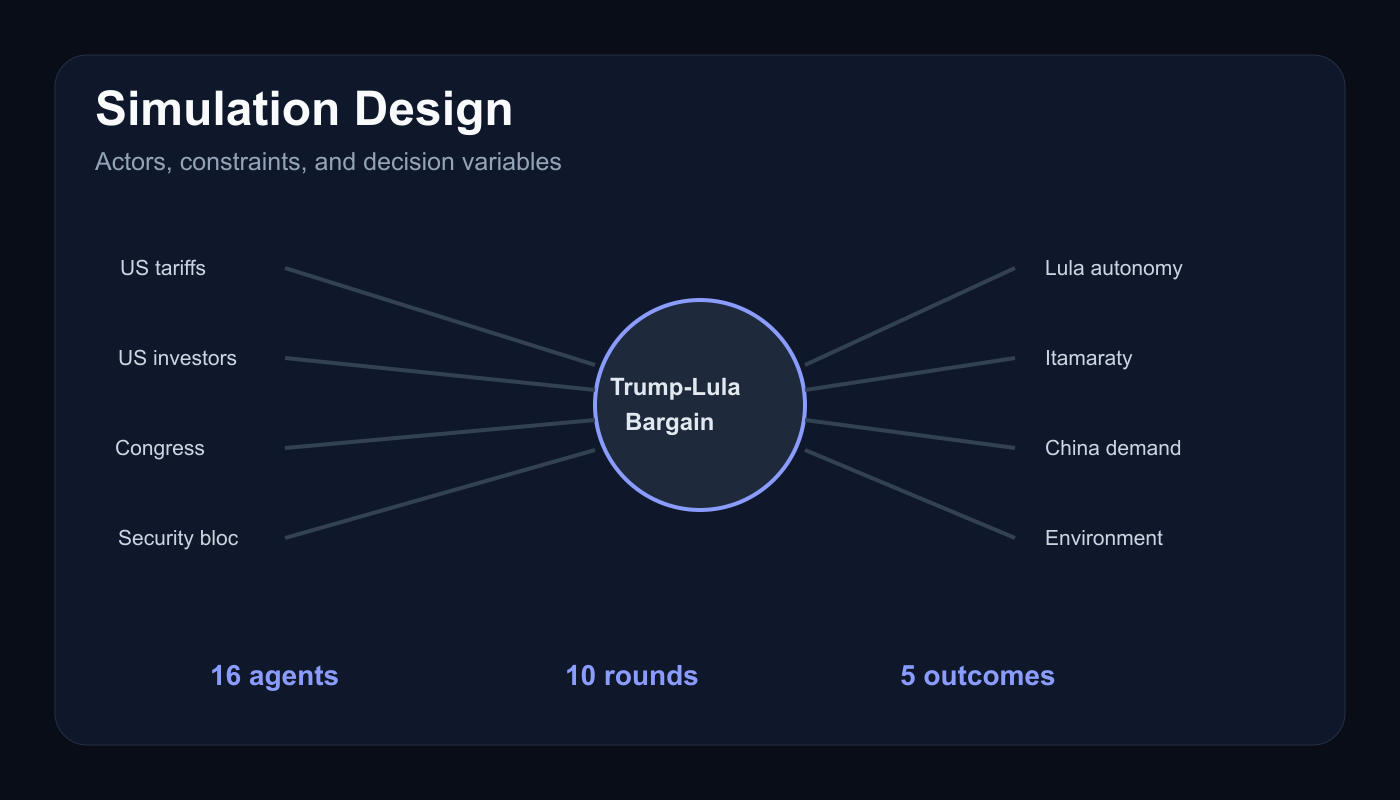

The MiroFish simulation used 16 agents and 10 rounds. It is an analytic simulation, not a poll, forecast market, or intelligence assessment. Each agent represented a stakeholder with incentives, constraints, and likely reaction functions. The agents debated whether the Trump-Lula meeting produces a practical bargain on tariffs, security, and critical minerals by June 30, 2026, or collapses into managed friction.

The agent set included Donald Trump, Luiz Inacio Lula da Silva, the US Trade Representative, a US Treasury and Commerce industrial-policy team, a Rubio-style hemispheric security bloc, Itamaraty, the Brazilian agribusiness lobby, the Brazilian mining and energy bloc, the Brazilian left coalition and PT base, China's Ministry of Commerce, Chinese commodity buyers, US Congress and protectionists, EU climate and trade actors, Brazilian environmental and Indigenous groups, US investors and mining firms, and Latin American regional governments.

The simulation modeled eight variables:

| Variable | Why it matters |

|---|---|

| Tariff threat intensity | Determines whether pressure creates concessions or backlash |

| Lula autonomy constraint | Determines how much cooperation Brazil can accept publicly |

| Critical minerals terms | Determines whether the package is bankable or symbolic |

| China reaction | Determines whether Beijing counters quietly through demand and diplomacy |

| Brazilian industry support | Determines whether agribusiness and mining lobby for pragmatism |

| US domestic politics | Determines whether Trump needs confrontation or a visible win |

| Environmental constraint | Determines whether Amazon extraction language becomes toxic |

| Regional security agenda | Determines whether Venezuela, crime, and migration become useful add-ons |

The output was a probability distribution across five outcomes, plus an assessment of the success factor, wildcard, cascade effects, and deal-killers.

Key Findings: US Brazil Tariffs and Non-Exclusive Minerals Cooperation

The final distribution is concentrated in the middle. The simulation does not expect a dramatic rupture. It also does not expect a clean strategic bargain. It expects a narrow package that gives each side enough to claim progress while avoiding language that makes the agreement domestically radioactive.

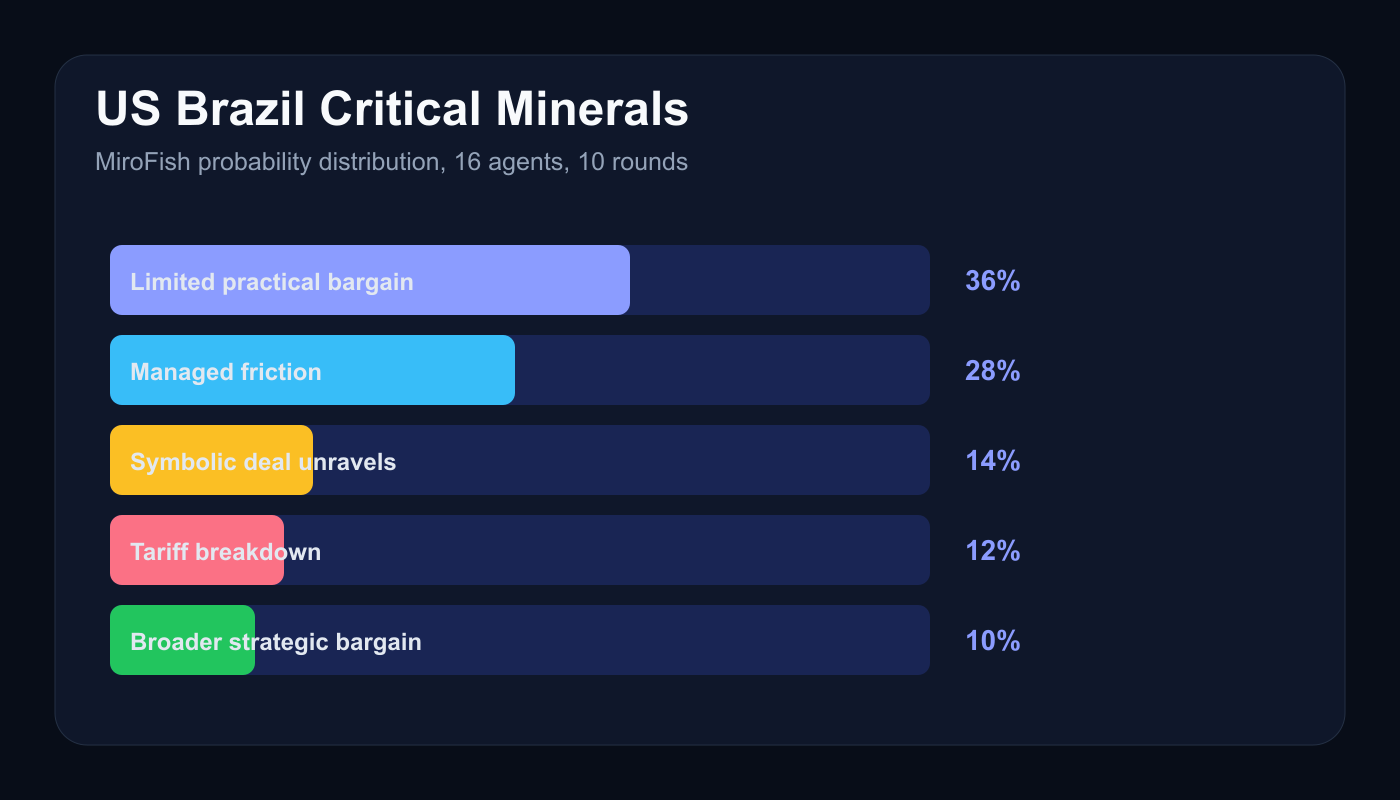

| Outcome by June 30, 2026 | Probability |

|---|---|

| Limited practical bargain with tariff pause and non-exclusive minerals/security framework | 36% |

| Managed friction with cordial communique but no meaningful deliverables | 28% |

| Symbolic grand-language deal that unravels under domestic and China pressure | 14% |

| Tariff/security breakdown leading to sharper US-Brazil tensions | 12% |

| Broader strategic bargain with enforceable tariff, minerals, and security commitments | 10% |

Brazil Critical Minerals Are the Bridge and the Trap

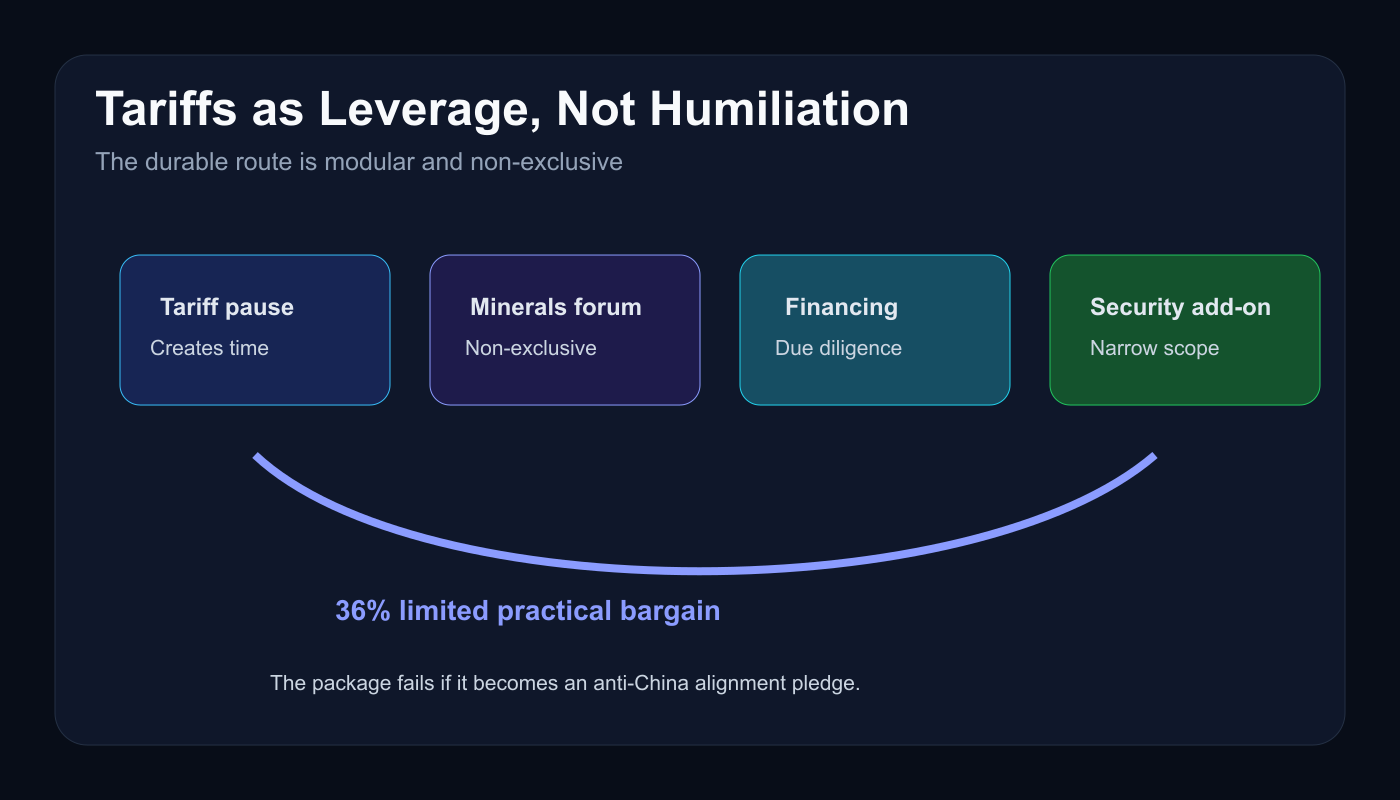

Brazil critical minerals cooperation is the strongest policy bridge because it lets the US talk about supply-chain resilience while letting Brazil talk about investment, processing, infrastructure, and value-added development. The trap is exclusivity. If the package implies that Brazil is reserving resources for Washington or helping contain China, it creates a domestic and diplomatic backlash.

The practical route is a non-exclusive framework: joint mapping, processing investment, financing channels, standards cooperation, recycling, port and rail infrastructure, and project-level due diligence. That structure lets US firms and agencies explore bankable projects without asking Lula to perform alignment politics.

Trump Lula Meeting Depends on Message Discipline

The biggest wildcard is not the text of the agreement. It is the post-meeting narrative. Trump benefits from saying he won. Lula benefits from saying Brazil preserved independence. Those claims can coexist only if the victory is framed as jobs, investment, tariff stability, and Western Hemisphere cooperation, not as Brazil choosing America over China.

If Trump publicly says Brazil conceded under tariff pressure, Lula has incentives to harden. If Lula's side emphasizes balanced diplomacy and practical investment, the agreement has room to survive. This is why the simulation assigns only 10% to a broader enforceable bargain. The politics can support a working group. They cannot easily support a treaty-like realignment.

US Brazil Tariffs Are Leverage, Not the Whole Deal

US Brazil tariffs matter because they create urgency. Brazilian agribusiness and industrial groups want certainty. US protectionists want reciprocity and visible concessions. But tariffs alone cannot produce the minerals outcome. Excess pressure can convert an economic bargain into a sovereignty fight.

The simulation's central path uses tariff restraint as the price of structured talks. A pause, exemption, or delayed escalation gives Lula a reason to engage. It gives Trump a visible tool. It gives investors time to evaluate projects. The failure path is straightforward: if tariffs become humiliation, Brazil hedges toward China and Europe while keeping the US relationship polite but shallow.

Market Implications: Critical Minerals, Agribusiness, and Capital Flows

The market implication is not an immediate mining boom. The 36% central outcome points to early-stage option value: due diligence, memoranda, financing discussions, and pilot projects rather than rapid extraction. Investors should treat the meeting as a signal that political doors may open, not as proof that permits, infrastructure, offtake agreements, and environmental approvals are solved.

Three sectors are most exposed.

First, mining and processing. The bankable opportunity is more likely in processing, infrastructure, recycling, and non-Amazon projects than in politically explosive raw extraction. Environmental and Indigenous groups were binding agents in the simulation. They pushed the deal away from loose extraction language and toward narrower investment categories with safeguards.

Second, agribusiness. Tariff certainty has direct value for exporters and logistics firms even if the minerals track remains exploratory. If the limited bargain holds, agribusiness becomes the domestic lobby that protects the relationship from ideological swings. If tariffs return, agribusiness pressure shifts toward hedging and alternative markets.

Third, industrial finance. US agencies, private miners, commodity traders, and infrastructure investors gain a reason to examine Brazilian projects that can diversify supply chains without requiring formal anti-China alignment. That is a narrower thesis than decoupling, but it is more credible. Capital can move through project finance, processing partnerships, logistics upgrades, and technology transfer.

Commodity price effects should be modest in the near term. A June 30 framework would not change global supply quickly. The more relevant pricing effect is risk premium. If the US and Brazil prove that mineral cooperation can happen without a public alignment fight, other middle powers gain a template. If the process collapses into tariff threats and sovereignty rhetoric, China-facing commodity routes look stickier.

Second-Order Effects: Will Brazil Choose the US or China on Critical Minerals?

The long-tail question, "will Brazil choose the US or China on critical minerals," has the wrong premise. The simulation's answer is no. Brazil's best move is to keep both doors open while extracting better terms from each side.

The first second-order effect is China acting quietly. Beijing does not need loud retaliation to shape the outcome. Commodity-demand signals, diplomatic reminders, procurement preferences, and infrastructure offers can make Brazilian officials cautious. The China agents in the simulation did not need to blow up the meeting. They only needed to make exclusivity expensive.

The second effect is regional signaling. Latin American governments will watch whether Brazil becomes a mediator, hedge, or US-aligned anchor. A non-exclusive deal gives other governments permission to accept US capital without joining an anti-China bloc. A coercive deal does the opposite. It teaches the region that Washington's offer comes with political costs.

The third effect is environmental politics. Any minerals package that smells like Amazon extraction without safeguards creates a domestic and international vulnerability. EU climate and trade actors can complicate green finance. Indigenous groups can turn a supply-chain deal into a sovereignty and rights fight. That does not kill cooperation. It moves cooperation toward processing, recycling, infrastructure, and tighter project selection.

The fourth effect is Trump's own narrative machinery. The simulation found that deal durability depends less on whether the leaders dislike each other ideologically and more on whether both can tell compatible stories. Trump needs strength. Lula needs autonomy. A modular bargain lets both stories be true.

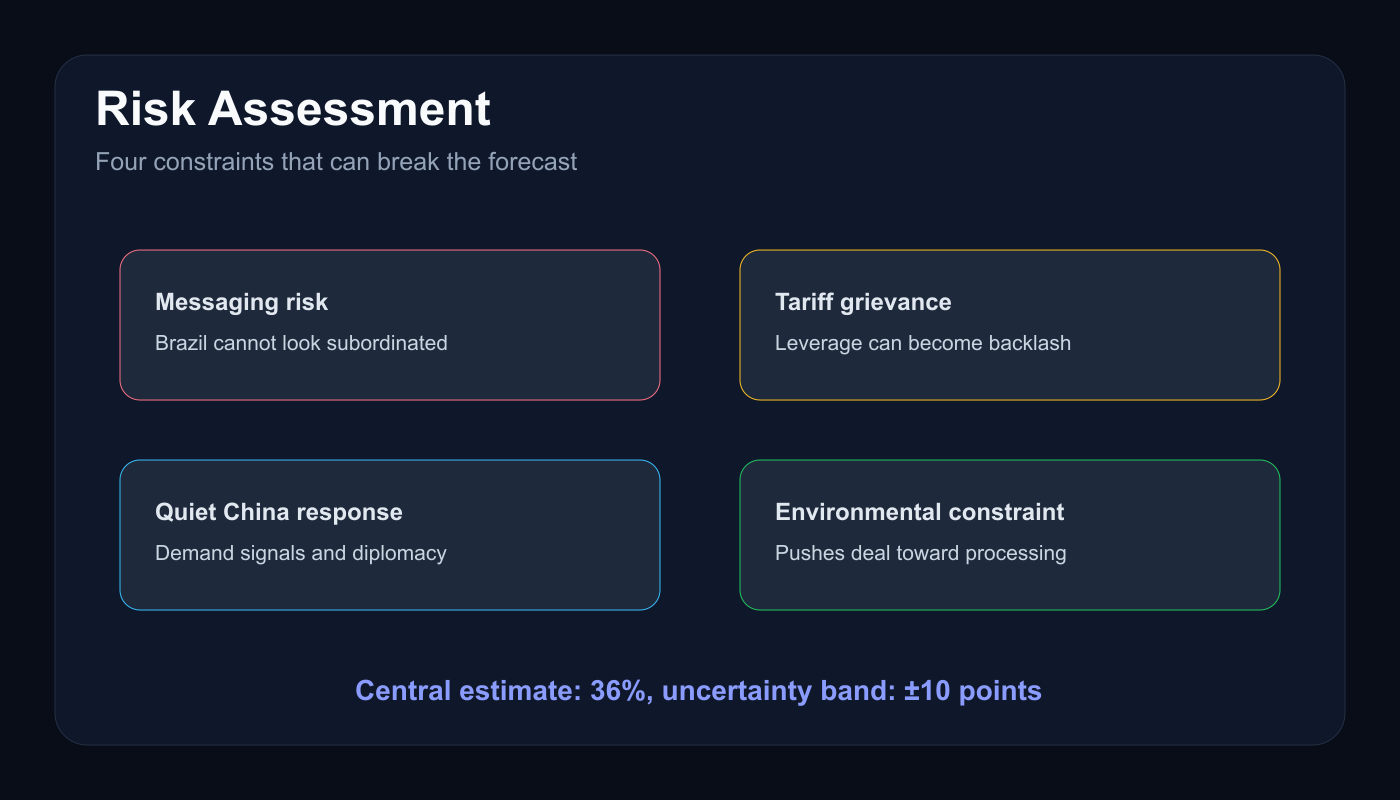

Risk Assessment: What Could Break the Forecast

The 36% central estimate should be read with an uncertainty band of roughly plus or minus 10 percentage points. Four risks dominate.

First, public messaging can outrun private terms. A workable draft can fail if either side oversells it. The most dangerous phrase is not technical. It is any public claim that Brazil joined a US anti-China supply-chain front.

Second, tariffs can switch from leverage to grievance. If US protectionists demand visible concessions, Lula's coalition can frame the deal as submission. That converts an economic negotiation into a sovereignty test.

Third, China can counter without escalation. Preferential buying, credit, investment, or diplomatic pressure can raise the cost of a US-facing framework. The simulation treats this as a slow constraint rather than a dramatic crisis.

Fourth, environmental and Indigenous politics can narrow the minerals track. This is not a marginal concern. It changes the feasible project set. Deals framed around processing and infrastructure are more durable than deals framed around raw extraction.

The downside case is not a total diplomatic rupture. It is managed friction: cordial language, no meaningful deliverables, renewed hedging, and a return to tariff uncertainty. That outcome receives 28%, close enough to the central case that execution matters more than press optics.

Conclusion

The Trump-Lula meeting is not a test of whether Brazil chooses the United States or China. It is a test of whether Washington can accept a deal that works precisely because Brazil refuses to choose.

The highest-probability outcome is a limited practical bargain: tariff restraint, non-exclusive minerals cooperation, financing talks, and narrow security language. That is enough to matter. It gives US investors a starting point, gives Brazilian industry tariff certainty, gives Trump a hemispheric win, and gives Lula a sovereignty-preserving story.

The strategic lesson is sharper than the headline. Critical minerals deals with middle powers will not be won by demanding alignment. They will be won by making non-exclusive cooperation more profitable, more bankable, and less politically costly than the alternatives. In this simulation, that is the path that survives.