Ukraine Drone Exports: 2026 Simulation

Ukraine drone exports are likely to become a narrow allied channel, with 44% odds of durable but limited wartime defense-tech sales.

Executive Summary

Ukraine drone exports are likely to become real by the end of 2026, but not as a broad arms-export boom. A 16-agent, 10-round MiroFish simulation assigns a 44% probability to the central outcome: a selective, donor-vetted export and co-production channel that is durable but limited. The framework works when exports are additive to Ukrainian battlefield supply, bundled with training and electronic-warfare integration, and routed through allied buyers such as Poland, the Baltics, and other eastern-flank states.

The simulation rejects the simple version of the story. Ukraine is not sitting on large pools of spare frontline systems. The exportable product is more likely to be a package: drones, counter-drone tools, software, maintenance, training, licensing, and co-production agreements funded by foreign buyers. That package lets Kyiv convert battlefield learning into industrial scale without visibly starving brigades at the front.

The key strategic finding is that the word "surplus" determines the whole policy. If "surplus" means extra production created by new capital, exports build Ukrainian influence. If it means scarce systems diverted from frontline units, the framework becomes politically explosive and operationally fragile.

Background and Context: Ukraine Weapons Export Policy

On April 28, 2026, Ukrainian reporting described President Volodymyr Zelenskyy's approval of a framework under which Ukraine could export surplus weapons and defense technology while continuing to prioritize its own army. The proposal matters because Ukraine's defense industry has changed under wartime pressure. Small drones, first-person-view systems, electronic warfare, battlefield software, counter-drone sensors, and cheap attritable platforms have moved from improvisation to a central part of modern combat.

That gives Ukraine an unusual position. It is a state under invasion, but also a laboratory for high-tempo defense technology. NATO members have spent heavily on conventional platforms, yet the war has shown that low-cost drones and rapid software iteration can change tactical economics. The result is demand for Ukrainian know-how, not only Ukrainian hardware.

Authoritative public sources support the context. NATO has emphasized innovation and interoperability through programs such as the Defence Innovation Accelerator for the North Atlantic. The European Union has pushed defense-industrial coordination through the European Defence Industrial Strategy. The Stockholm International Peace Research Institute tracks the global arms-transfer market that Ukraine is trying to enter under wartime constraints. Ukraine's own policy discussion sits inside this larger move toward rapid procurement, joint production, and battlefield-tested systems.

The constraint is equally clear. Ukraine's brigades still need drones, munitions, sensors, vehicles, and electronic-warfare equipment every day. Donor governments also retain leverage because many systems include US, EU, or NATO-origin components, software, chips, optics, radios, or encryption. Export controls are not a detail. They can decide whether the framework becomes a bilateral Ukrainian market, a NATO-aligned co-production channel, or a paper policy with limited actual sales.

This post extends the research line on Zeki's simulation desk, including prior geopolitical and defense-industry scenario work at zekiai.xyz/blog. The question here is narrower than whether Ukraine can become a major arms exporter someday. The question is whether Ukraine can create a durable wartime revenue-and-influence channel before the end of 2026.

Methodology: Ukraine Defense Tech Simulation Design

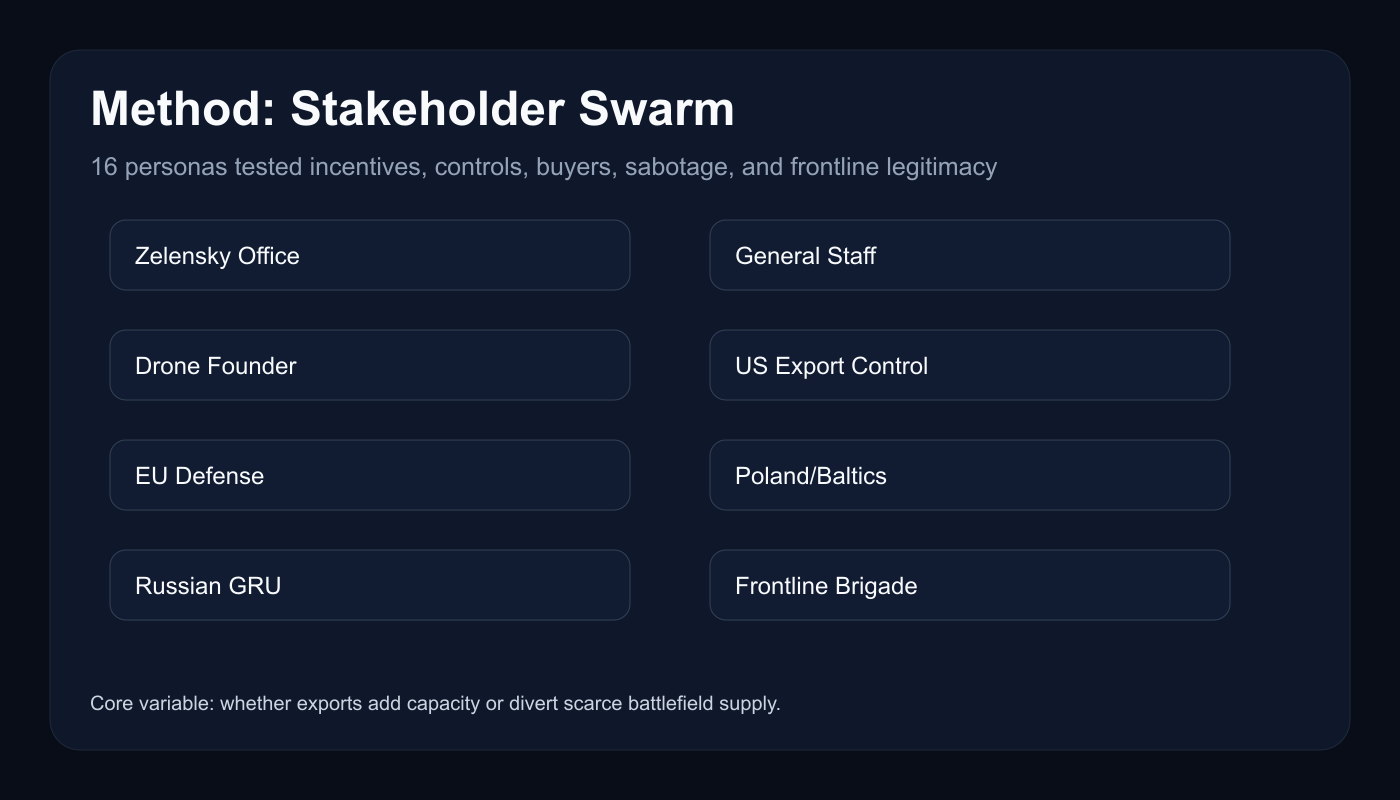

The MiroFish simulation used 16 agents and 10 rounds. It is an analytic simulation, not a prediction market and not an intelligence assessment. Each agent represented a stakeholder with incentives, constraints, and likely reactions. The agents debated whether Ukraine's export framework becomes durable by end-2026 or is blocked by battlefield demand, donor controls, and escalation risk.

The agent set included: the Zelensky Office, Ukrainian General Staff, Ukrainian drone founder, Ministry of Strategic Industries, US State and Commerce export-control official, Pentagon procurement strategist, EU defense commissioner, Polish and Baltic security buyer, Gulf defense buyer, Israeli defense-tech executive, Turkish defense-industry strategist, Russian GRU sabotage planner, Chinese defense analyst, Western defense prime lobbyist, anti-corruption and end-use monitor, and frontline Ukrainian brigade commander.

The simulation modeled eight variables:

| Variable | Why it matters |

|---|---|

| Battlefield scarcity | Determines whether exports are politically credible |

| Donor/export-control limits | Determines whether sales are allowed and monitorable |

| Buyer demand | Determines whether foreign revenue is large enough to scale production |

| Russian response | Determines sabotage, cyber, legal, and intimidation risk |

| Industrial scaling | Determines whether exports add capacity instead of redirecting supply |

| Governance and trust | Determines whether scandals freeze donor tolerance |

| NATO interoperability | Determines whether Ukraine becomes a supplier or subcontractor |

| Political narrative | Determines whether exports are viewed as self-financing or betrayal |

The output is a probability distribution across five end-2026 outcomes, plus a qualitative assessment of turning points, deal-killers, second-order effects, and market implications.

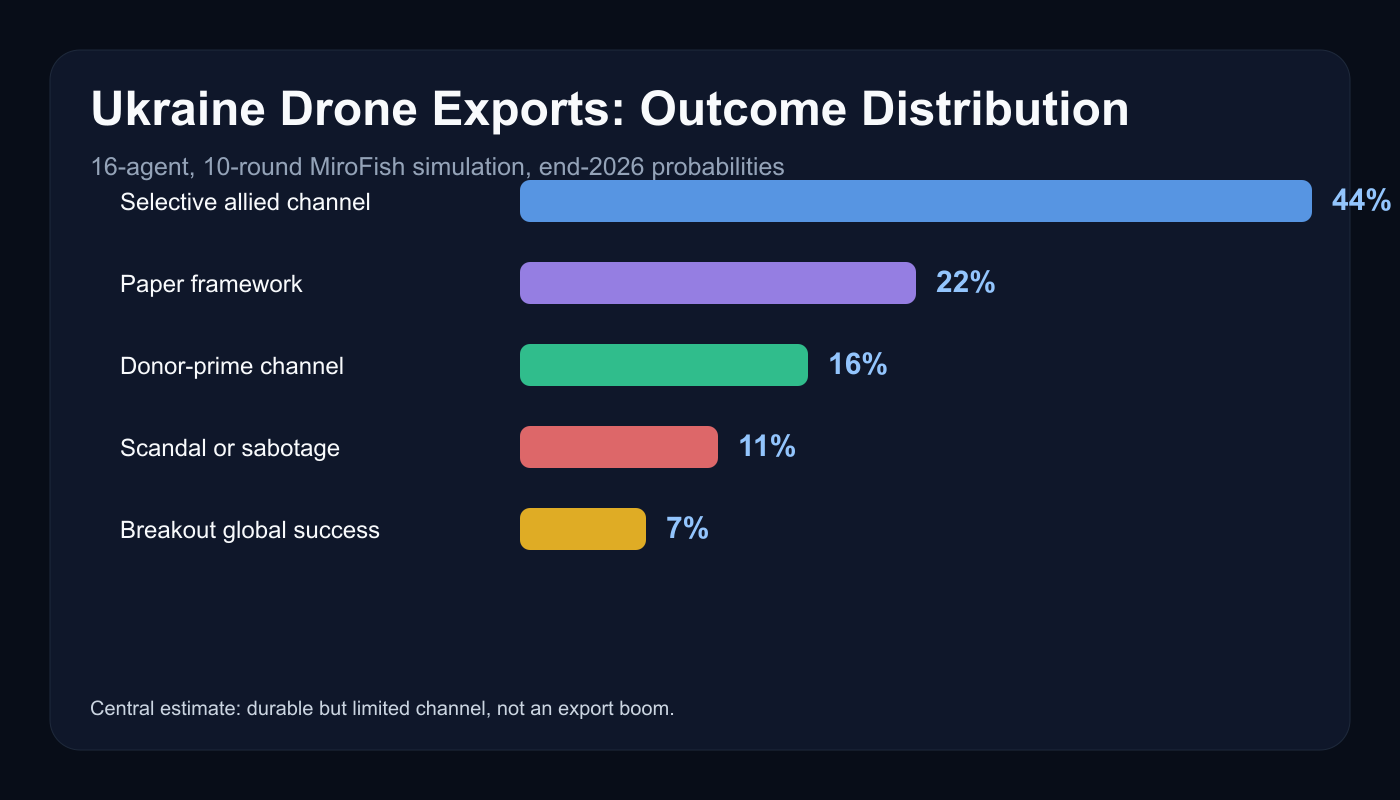

Key Findings: Ukraine Drone Exports Are Durable but Limited

The final distribution was not polarized. The swarm did not converge on either an export boom or a failed announcement. It converged on a narrow channel.

| Outcome by end-2026 | Probability |

|---|---|

| Selective allied export/co-production channel becomes durable but limited | 44% |

| Framework exists mostly on paper due to battlefield scarcity and backlash | 22% |

| Donor/export-control regime channels Ukraine into Western prime or EU-led programs | 16% |

| Corruption, diversion, security scandal, or Russian sabotage chills the program | 11% |

| Breakout export success beyond NATO and eastern-flank buyers | 7% |

Ukraine Weapons Export Depends on the Meaning of Surplus

The most important finding is definitional. Durable Ukraine weapons export policy depends on proving that exported systems are surplus because capacity has expanded, not because the front has accepted less supply. The Ukrainian General Staff and frontline brigade agent both resisted broad exports unless every item fell into one of three categories: genuinely surplus, no longer tactically relevant, or produced through foreign-funded additional capacity.

That distinction changes the commercial model. If a Polish or Baltic buyer funds a new line, licensing package, training team, or co-production facility, the export can increase total output. If a buyer simply takes drones from existing Ukrainian production, the domestic political narrative becomes toxic. The simulation treated frontline legitimacy as a binding constraint, not a communications problem.

Ukraine Defense Tech Buyers Favor the Eastern Flank

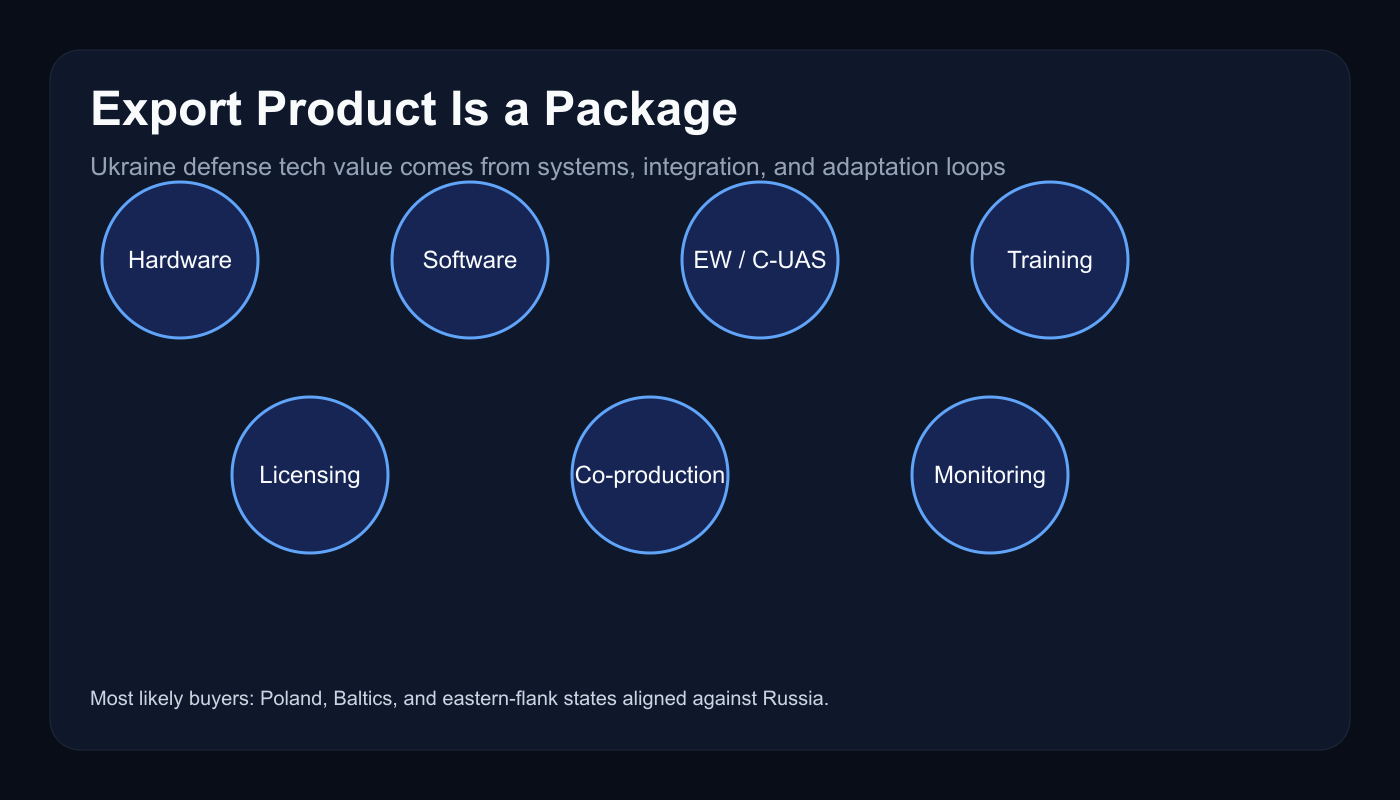

The second finding is that early buyers are not necessarily the richest buyers. Gulf states have money and may want battlefield-tested drone and electronic-warfare systems, but the simulation ranked Poland, the Baltics, and other eastern-flank customers as the more likely first channel. Their threat perception aligns with Ukraine's. Their purchases fit donor politics. Their procurement rationale is easy to defend: systems proven against Russia are most relevant to states exposed to Russian pressure.

This matters for revenue expectations. Eastern-flank demand may be politically durable, but it is also more likely to be structured through monitored allied programs, EU mechanisms, or NATO-compatible procurement. That reduces scandal risk and improves interoperability, but it also limits the unconstrained margin profile that a pure global export boom might imply.

Drone Warfare Ukraine Lessons Become an Export Package

The simulation did not treat drones as standalone commodities. The stronger export product is a kill-chain and adaptation package: airframes, software, electronic warfare, counter-drone detection, maintenance, operator training, tactical lessons, and rapid upgrade loops. That is what foreign buyers want from drone warfare Ukraine experience.

This is also where Ukraine can defend the policy domestically. Selling a training and co-production package does not carry the same political cost as shipping scarce frontline drones abroad. It lets Ukrainian firms scale production, professionalize support, and lock in foreign customers while keeping battlefield priority credible.

Market Implications: Defense Industry, Procurement, and Capital

The market implication is not that Ukraine instantly becomes a top-tier arms exporter. The implication is that wartime innovation becomes investable and procurement-relevant. A 44% durable-but-limited outcome means capital should look for hybrid structures: Ukrainian design plus allied financing, local assembly, NATO-compatible interfaces, and clear end-use monitoring.

Three markets are most exposed.

First, European defense procurement. If eastern-flank states buy Ukrainian systems or co-produce them, European procurement cycles face pressure to become faster. Cheap drones and electronic-warfare tools will not replace tanks, air defense, or artillery. They will change the required ratio between expensive platforms and cheap attritable mass.

Second, Western defense primes. The simulation's Western prime lobbyist did not expect Ukrainian firms to be left alone if they gain export traction. The likely response is partnership, acquisition, integration into larger procurement packages, or lobbying for standards that route Ukrainian technology through prime-led programs. This is why the 16% donor-channel outcome matters. It is not failure. It is institutional absorption.

Third, venture and defense-tech capital. Ukraine's wartime startups can become more financeable if export contracts create predictable revenue. But investors should discount companies that depend on uncontrolled exports outside allied channels. The realistic upside lies in verified supply chains, component substitution away from vulnerable inputs, cybersecurity, training, and lifecycle support.

Price effects are harder to quantify than procurement effects. The simulation does not imply immediate changes in oil, gold, or shipping markets. It does imply a longer-term repricing inside defense budgets: more funding for drones, electronic warfare, low-cost interceptors, sensors, and battlefield software. If Ukraine proves that these systems can be exported with control and accountability, allied defense spending shifts toward scalable consumables and software-defined upgrades.

Second-Order Effects: What the Headline Misses

The first second-order effect is diplomatic. Ukraine can use defense exports as security diplomacy. A country that buys Ukrainian systems is not just buying equipment. It is linking itself to Ukraine's wartime supply chain, training base, and anti-Russian security narrative. For eastern-flank states, that link is strategically coherent. For nonaligned buyers, it is more complicated.

The second effect is Russian active measures. The Russian GRU sabotage agent treated the export framework as a threat worth attacking. The cheapest way to chill the program is not necessarily a missile strike on a factory. It is a diversion allegation, cyber breach, fake corruption scandal, intimidated buyer, or leak that makes donors fear uncontrolled technology transfer. The 11% scandal or sabotage outcome is small enough to be secondary, but large enough to shape policy design.

The third effect is component politics. A successful export framework reveals supply chains. If Ukrainian systems depend on Chinese dual-use components, Western export-control officials will push for substitution, monitoring, or restrictions. That creates a new market for resilient components and trusted electronics, but it also slows scale.

The fourth effect is domestic legitimacy. If frontline units report better supply while exports begin, the policy looks like clever self-financing. If frontline units crowdfund drones while the government announces foreign sales, the framework becomes politically brittle. This is the strongest if-then in the simulation: if brigades feel increased supply first, exports can grow. If they do not, the policy stalls.

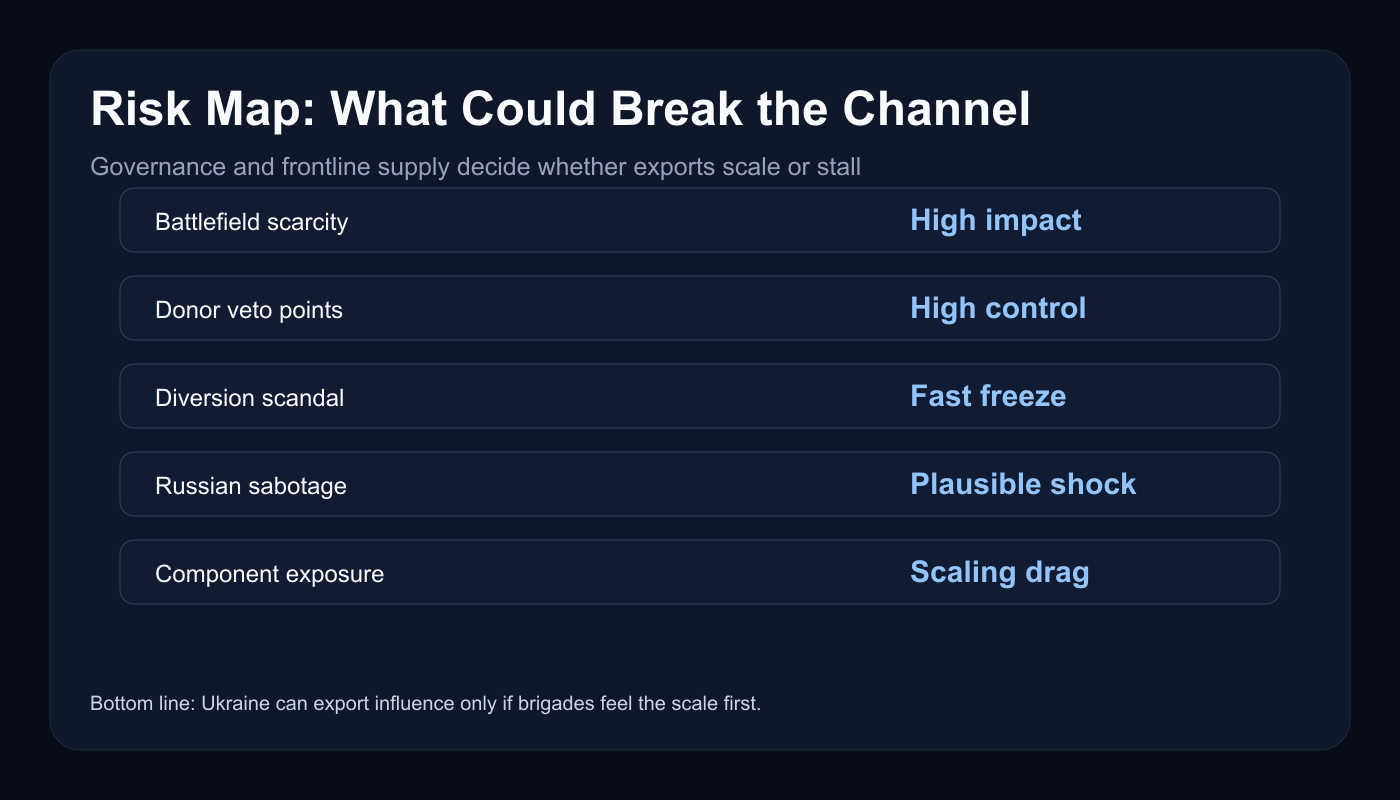

Risk Assessment: What Could Break the Forecast

The 44% central estimate should be read with a wide uncertainty band, roughly plus or minus 12 percentage points. The simulation depends on policy execution, battlefield conditions, donor tolerance, and Russian disruption. Four risks dominate.

First, battlefield demand may rise faster than industrial capacity. A major Russian offensive, drone attrition spike, or munition shortage would make exports harder to justify, even if contracts are politically attractive.

Second, donor controls may be stricter than expected. US-origin components, EU rules, encryption, sensors, and dual-use software can create veto points. This risk does not necessarily kill the framework. It pushes it toward Western prime, EU, or NATO-managed channels.

Third, governance risk is non-trivial. A real diversion case, or a plausible fake amplified well, can freeze donor support. End-use monitoring and transparent category rules are not bureaucratic extras. They are commercial infrastructure.

Fourth, buyer risk tolerance may be overstated. Gulf and Asian buyers may study Ukrainian systems but hesitate to buy visibly during the war because of Russian or Iranian retaliation risk, supply continuity concerns, or diplomatic balancing.

Conclusion

Ukraine drone exports are most likely to become a narrow but durable allied channel by the end of 2026. The winning model is not broad shipment of scarce weapons. It is additive capacity: co-production, licensing, training, electronic-warfare integration, software, and monitored sales to buyers whose threat model aligns with Ukraine's war.

The actionable takeaway is simple. Watch the first buyers and the first governance rules. If the early deals are eastern-flank, donor-vetted, and tied to new production capacity, the 44% central case strengthens. If the first controversy is about frontline shortages, diversion, or uncontrolled components, the framework moves toward the 22% paper-policy or 11% scandal outcomes.

Ukraine can export influence while fighting Russia, but only if its soldiers feel the scale first.