US China Trade Truce: 60-Day Risk Simulation

US China trade truce simulation finds 38% managed-truce base case, 31% sector retaliation risk, and Iran sanctions as the key trigger.

Executive Summary

US China trade truce risk is moving below the tariff headline. A 16-agent, 10-round MiroFish simulation found a 38% probability that the truce survives formally over the next 60 days while degrading in substance through deniable Chinese pressure. The second most likely outcome, at 31%, is a sector-specific retaliation cycle involving aviation, agriculture, critical inputs, licensing, shipping, or sanctions compliance. The key result is blunt: the truce is more likely to be hollowed out than openly broken.

The simulation's most important variable is whether Beijing keeps pressure deniable and targeted enough for the Trump White House to treat it as bargaining behavior rather than public cheating. If China uses customs pressure, informal boycotts, export controls, or licensing delays without creating a visible market shock, the truce can remain politically alive. If a pressure tactic hits Boeing, farm states, rare earth users, insurers, or a China-linked Iran sanctions target, the system can move rapidly from managed rivalry to retaliatory escalation.

The base case is not stability. It is controlled deterioration. Washington preserves the language of a truce because markets, corporate lobbies, and Treasury stabilizers want a ceiling on tariff escalation. Beijing preserves the language of a truce because a broad tariff spiral would damage growth and narrow its own options. But both sides continue searching for tools that impose pain without admitting escalation. That makes the next 60 days less about a signed agreement and more about whether coercive ambiguity can stay contained.

Background and Context: China Economic Coercion

The simulation was seeded from a current tension: reports that China is expanding its economic pressure toolkit while operating under the political cover of a trade truce. The issue is not whether the United States and China are competitors. That is settled. The issue is whether both governments can keep competition inside a managed channel when each side has incentives to test the other below the formal threshold of truce violation.

China's economic coercion toolkit has become more modular. It can include selective customs scrutiny, delayed approvals, export controls, licensing uncertainty, informal consumer pressure, state-media signaling, procurement pressure, anti-monopoly or data-security investigations, and pressure on foreign firms with China exposure. These tools are useful because they can be denied, narrowed, or reversed. They also create asymmetric pressure: a public tariff is visible to everyone, while a delayed part, held shipment, suspended certificate, or unexplained purchasing pause can affect one company or sector before becoming a diplomatic event.

The U.S. side has its own layered toolkit. Tariffs remain the most visible instrument, but sanctions, export controls, investment restrictions, customs enforcement, and entity listings increasingly shape the contest. The Office of the U.S. Trade Representative provides the public record for tariff actions under Section 301. The U.S. Treasury sanctions database and press releases show how financial measures can target networks tied to Iran, Russia, shipping, and procurement. The Bureau of Industry and Security is the institutional reference point for export-control pressure.

That overlap matters because trade disputes rarely stay inside one file. A China-linked Iran oil sanction can become a trade-truce stressor. A rare earth licensing delay can become a technology escalation. A Boeing delivery disruption can become a political symbol. A soybean purchasing slowdown can become a farm-state problem. The simulation should be read as a study of transmission channels, not just trade diplomacy.

Zeki's prior simulations at zekiai.xyz/blog repeatedly found that the most dangerous shocks are not the largest official moves. They are cross-domain collisions. The Russia crypto sanctions simulation showed how enforcement pressure migrates through financial plumbing. The China, Panama, and Iran simulation showed how shipping, sanctions, and geopolitical signaling interact. This US-China case follows the same pattern: the headline is trade, but the stress points are aviation, energy sanctions, critical inputs, and market confidence.

Methodology: Will the US China Trade Truce Survive 2026?

This paper is based on a structured MiroFish-style multi-agent simulation. It is not a poll, classified assessment, or prediction market. Sixteen agents were run through ten rounds. Each agent represented an institution or pressure node with its own incentives, limits, and escalation threshold. The simulation question was: over the next 60 days, does the US-China trade truce hold as managed rivalry, or does China's economic pressure campaign trigger a wider breakdown?

The 16 agents were:

- Trump White House Trade Hawk

- U.S. Treasury and Markets Stabilizer

- USTR Tariff Strategist

- U.S. Sanctions Official

- Boeing and Aerospace Lobby

- U.S. Farm-State Senator

- Xi and Chinese Central Leadership

- Chinese Commerce Ministry

- Chinese Nationalist Media Ecosystem

- Chinese Export-Control Bureau

- EU Trade Commissioner

- Japanese and South Korean Tech Supply Chain Planner

- Iranian Oil and Shadow Trade Network

- Global Shipping and Insurance Market Analyst

- Multinational CEO in China

- Market Macro Fund Manager

The round structure forced agents to react to the same events from different institutional positions. U.S. hawks tested whether Chinese pressure should be framed as truce cheating. Treasury and market actors tried to preserve the truce as a stabilizing device. Chinese leadership sought pressure without uncontrolled crisis. Chinese commerce and export-control agents searched for deniable leverage. Boeing, agriculture, shipping, and insurance actors translated policy into corporate pain. Allied agents evaluated whether to align with Washington, hedge, or avoid a forced-choice confrontation.

The value of this method is structured friction. A single analyst can produce a clean narrative. A multi-agent process makes clean narratives harder. The USTR actor sees enforcement. The Treasury actor sees market risk. The Chinese nationalist media actor sees concession costs. The Boeing lobby sees delivery and maintenance exposure. The farm-state senator sees election pressure. The insurer sees compliance risk before diplomats agree on language. The output is therefore a map of incentive collisions.

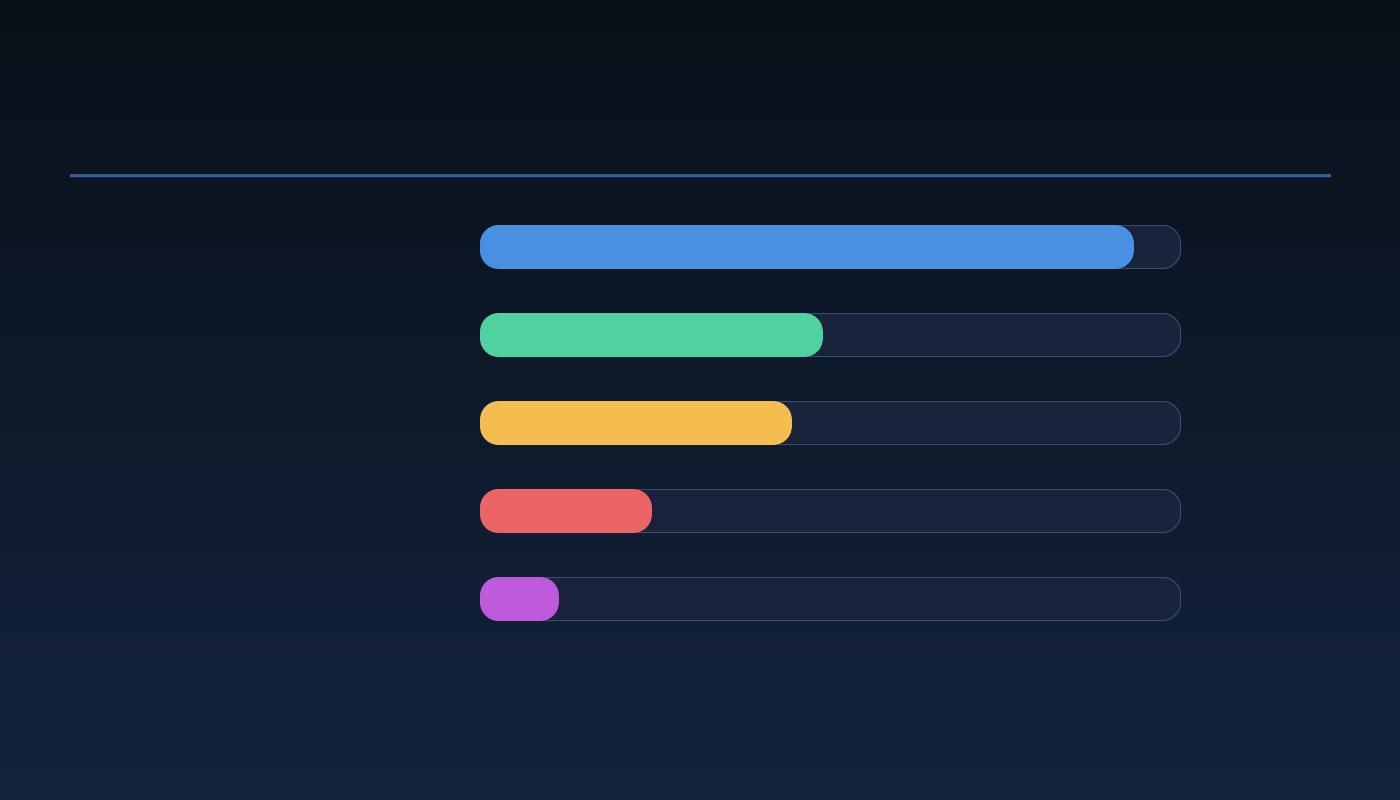

Key Findings: US China Trade Truce Probability

The final probability distribution was:

| Scenario over the next 60 days | Probability | Core mechanism |

|---|---|---|

| Managed truce with deniable Chinese pressure | 38% | The truce survives formally while pressure shifts to targeted tools |

| Sector-specific retaliation cycle | 31% | Aviation, agriculture, export controls, or licensing becomes public |

| Iran-sanctions trigger breaks the truce | 14% | A China-linked sanctions event becomes a political flashpoint |

| Market shock forces de-escalation | 10% | Equities, shipping, oil, or corporate stress forces a cooling move |

| Broad tariff or trade-war relapse | 7% | Both sides return to overt tariff escalation |

China economic coercion keeps the truce alive and weaker

The highest-probability outcome is paradoxical: the truce survives because it becomes less meaningful. Beijing has incentives to avoid a broad tariff spiral, but it also has incentives to show that Washington cannot pocket a truce while continuing sanctions, technology controls, and alliance pressure. Deniable economic coercion solves that problem. It allows China to impose costs while preserving the option to say nothing has changed.

This is why the simulation did not rank broad tariff relapse as the base case. Formal tariffs are noisy, legally and politically visible, and quickly priced by markets. Targeted friction is more flexible. A certification delay, a customs inspection wave, a procurement pause, or a licensing holdup can be escalated or reversed without a dramatic announcement. That flexibility is useful for policymakers and dangerous for companies.

China rare earth export controls raise the ceiling

China rare earth export controls and critical-input licensing were treated as escalation ceiling tools rather than first moves. Their importance is that they give Beijing leverage over downstream industries that are politically sensitive in the United States, Japan, South Korea, and Europe. The U.S. Geological Survey tracks the structural importance of rare earths, while the International Energy Agency documents how critical minerals shape energy and technology supply chains.

The simulation found that critical-input pressure is most dangerous when paired with another dispute. Rare earth restrictions alone can be framed as export-control policy. Rare earth restrictions after a sanctions designation, tariff threat, or public presidential accusation become proof of retaliation. That sequencing risk is the core issue. The same act can be manageable or escalatory depending on what came before it.

China Iran sanctions are the cleanest trigger

China Iran sanctions produced the sharpest truce-break pathway. Washington can frame sanctions against China-linked Iran oil trade as legal enforcement rather than trade escalation. Beijing can frame the same action as bad-faith pressure during a truce. That disagreement gives both sides a plausible public story, which makes escalation easier.

The wildcard identified by the simulation was a sanctions event tied to a major Chinese firm, bank, shipper, insurer, or strategic industrial player. If the target is small, both sides can compartmentalize. If the target is symbolically large or systemically connected, Chinese retaliation becomes harder to avoid. The retaliation would likely appear first in sectors where Beijing can apply pain without declaring it: aviation, agriculture, licensing, procurement, or critical inputs.

Market Implications: Boeing, Soybeans, Shipping, and Risk Assets

The simulation's market message is that investors should watch sector channels before tariff headlines. The truce can degrade for weeks before a public breakdown. That degradation would show up first in corporate guidance, delivery timelines, customs anecdotes, insurance language, trade-finance caution, and commodity flows.

Aviation is the cleanest visibility channel. Boeing is symbolically important, economically large, and politically legible. Delivery delays, certification friction, parts issues, or airline purchasing signals would quickly become a Washington story. That does not mean aviation pressure is the most likely first move. It means aviation pressure has the fastest path from bureaucratic friction to political escalation.

Agriculture is the domestic-political channel. Soybeans and farm exports convert foreign retaliation into local pressure. A Chinese purchasing slowdown can be described as commercial, but U.S. farm-state politicians would treat it as strategic. This makes agriculture a powerful accelerant even when the dollar amount is smaller than technology or aviation exposure.

Shipping and insurance are the early-warning channels. If China Iran sanctions expand, compliance teams and insurers may tighten before governments announce the next move. That can raise transaction costs, delay shipments, and create a market narrative around hidden escalation. The EIA's oil market analysis is useful context for energy-linked sensitivity, while public Treasury sanctions notices provide the enforcement baseline.

For risk assets, the base case is intermittent repricing rather than a single shock. Equities can tolerate a formal truce with noise. They struggle with uncertainty about which sector is next. The market-shock de-escalation scenario received only 10% because markets usually brake escalation after pain becomes visible, not before. In practical terms, the market is a feedback mechanism, not a preventive institution.

Second-Order Effects: How a Formal Truce Fails Informally

The most important second-order effect is normalization. If both sides accept deniable pressure as compatible with the truce, the truce becomes a container for coercion rather than a constraint on it. That can work for a short period. It is unstable over longer periods because each side keeps testing what the other will tolerate.

If Beijing targets one sector quietly, Washington can respond privately. If Beijing targets multiple sectors, private response becomes politically insufficient. If Washington answers with sanctions or export controls, Beijing can claim the United States broke the spirit of the truce. If markets sell off, both sides can step back while blaming misunderstanding. If markets do not sell off, escalation pressure continues.

Allied behavior is another second-order effect. The EU, Japan, and South Korea dislike Chinese coercion but also dislike being forced into a U.S.-China binary. The simulation found hedging as the dominant allied posture. Allies would coordinate selectively on coercion and supply-chain resilience, but avoid signing up for every U.S. retaliation package. That limits Washington's leverage and encourages Beijing to keep pressure targeted.

Nationalist media is the final constraint. Once a dispute becomes public, backing down becomes harder for Beijing and Washington. The simulation repeatedly pushed both governments toward private warnings, procedural delays, and ambiguous language because visible humiliation is expensive. The more public the accusation, the less room both sides have to preserve the truce.

Risk Assessment: What Could Be Wrong

The simulation may understate the chance of rapid de-escalation if senior leaders decide the economic risk is too high. A single phone call, negotiated carveout, or quiet licensing fix could neutralize a sector shock before it becomes public. That is the strongest argument for a more benign outcome.

It may also understate the chance of broad tariff relapse if the White House concludes that ambiguity itself is the problem. If Trump frames deniable Chinese pressure as cheating, the distinction between targeted coercion and formal truce violation collapses. In that world, a small sector incident can become a test of credibility.

A third uncertainty is data visibility. Deniable pressure is hard to measure in real time. Customs friction, purchasing pauses, inspections, informal guidance, and licensing delays often appear as scattered corporate anecdotes before they appear as official policy. This means the first public signals may lag the actual escalation.

The confidence band around the top two outcomes should be treated as wide. Managed deterioration at 38% and sector-specific retaliation at 31% are close enough that a single event can swap their order. The robust conclusion is not the exact ranking. It is that controlled, sectoral, deniable pressure is far more likely than immediate broad tariff war.

Conclusion

The US China trade truce is most likely to survive on paper and weaken in practice. The simulation's 38% base case is a managed truce with deniable Chinese pressure. The 31% near-base case is a sector-specific retaliation cycle. Together, those outcomes define the real forecast: the next 60 days are not about peace versus trade war. They are about whether coercive ambiguity stays below the political threshold.

The practical signal set is clear. Watch Boeing and aviation procedures. Watch soybean and agricultural purchasing. Watch China Iran sanctions designations. Watch rare earth and critical-input licensing. Watch shipping and insurance compliance language. Watch whether allies coordinate or hedge. A truce breakdown will probably not begin with a dramatic tariff announcement. It will begin as a company problem, a shipment problem, a sanctions problem, or a licensing problem that becomes impossible to keep private.

The actionable takeaway is simple: treat the formal truce as a ceiling on overt escalation, not as evidence of strategic calm. The rivalry is not paused. It has moved into quieter instruments. Those instruments are harder to see, harder to price, and harder to stop once they collide with domestic politics.