US Iran Talks: Hormuz Escalation Risk

US Iran talks simulation finds 42% coercive stalemate risk as Pakistan and Oman channels compete with Strait of Hormuz escalation pressure.

Executive Summary

US Iran talks are no longer a clean diplomatic question. They are now competing with a commercial escalation ladder built around the Strait of Hormuz, Iran oil sanctions, shipping insurance, and shadow trade enforcement. A 16-agent, 10-round MiroFish simulation found a 42% probability that the crisis settles into coercive stalemate by 2026-05-10: threats continue, sanctions tighten, maritime warnings persist, and Pakistan or Oman carries intermittent backchannel messages, but neither side secures a visible breakthrough or triggers a sustained Hormuz confrontation.

The key finding is that the Pakistan channel is wounded, not dead. The reported cancellation of envoy travel damages public momentum, but it does not eliminate the need for a deniable message carrier. Oman likely complements Pakistan rather than replacing it. The market danger is that insurers, shippers, and oil traders move before diplomats do. That makes the crisis less about official statements and more about second-order signals: war-risk premiums, vessel advisories, Chinese buyer exposure, escort demands, port security, and shadow tanker enforcement.

The simulation's base case is not peace. It is pressure with guardrails. Washington can satisfy hawkish demands through sanctions and posture. Tehran can preserve deterrent ambiguity around Hormuz without formally closing the strait. Gulf states, China, and commercial actors then act as the limiting system. The danger is that this limiting system can also become the accelerant if one ambiguous vessel incident forces everyone to price crisis before facts stabilize.

Background and Context: Strait of Hormuz Risk

The Strait of Hormuz is the narrow maritime hinge between Gulf energy exports and global markets. The U.S. Energy Information Administration describes it as one of the world's most important oil chokepoints, with a large share of seaborne oil and liquefied natural gas moving through or near the channel. That is why threats around Hormuz matter even when no closure occurs. The market does not need a blockade to reprice risk. It needs credible uncertainty about transit reliability.

The current crisis, as modeled in the simulation seed, has two overlapping tracks. The first is a diplomatic track involving Pakistan and Oman as potential intermediaries between Washington and Tehran. Pakistan has visibility but also political exposure. Oman has a longer record as a quiet backchannel and can operate with less public theater. The second track is coercive and commercial: U.S. sanctions pressure, Iran-linked maritime signaling, shipping advisories, insurance repricing, Chinese purchases of Iranian oil, and Gulf port vulnerability.

That structure matters because escalation can occur without a deliberate decision to start a war. A sanctions package can push Iranian-linked trade networks toward riskier routing. A warning from Iranian hardliners can make a shipping line review exposure. An ambiguous incident involving a commercial vessel, shadow-fleet tanker, drone, or patrol boat can cause underwriters to raise premiums. Once premiums move, the price action becomes a political fact.

The broader research pattern is visible across Zeki's prior simulations at zekiai.xyz/blog. The earlier Strait of Hormuz crisis simulation found that diplomatic off-ramps remain plausible because regional actors fear owning the first obvious step into an energy shock. The US-Iran nuclear deal simulation similarly found that face-saving sequencing often matters more than maximalist public rhetoric. This simulation updates that logic for a more commercially charged setting.

Authoritative external baselines reinforce the stakes. The EIA's Strait of Hormuz analysis explains why even partial disruption risk matters to energy markets. The U.S. Treasury press releases provide the public record for sanctions designations and enforcement language. The International Atomic Energy Agency's Iran page remains the technical reference point for nuclear monitoring context that shapes diplomatic leverage.

Methodology: Iran Pakistan Talks and MiroFish Simulation

This paper is based on a structured MiroFish-style multi-agent simulation, not classified reporting, polling, or a prediction market. Sixteen agents were run through ten rounds. Each agent represented an institution with a goal, fear threshold, and strategic bias. The simulation question was: by 2026-05-10, does the US-Iran crisis move back into Pakistan-mediated talks, escalate into a wider maritime and trade confrontation, or settle into coercive stalemate?

The 16 agents were:

- Trump NSC Hawk

- U.S. Treasury Sanctions Architect

- U.S. CENTCOM Commander

- Iran Supreme Leader Adviser

- IRGC Naval Commander

- Iran Foreign Ministry Pragmatist

- Pakistan Mediator

- China Energy Security Planner

- UAE Ports and Trade Official

- Saudi Security Adviser

- Oman Backchannel Diplomat

- Israel Security Cabinet Member

- MSC Shipping Executive

- Lloyd's War Risk Underwriter

- EU Energy and Trade Official

- Global Oil Trader

Each round forced agents to react to the cancelled envoy travel report, Hormuz threats, Treasury's sanctions logic, Gulf state restraint, Pakistan's effort to remain useful, Oman's quieter mediation role, shipping and insurance behavior, Israeli pressure against a premature off-ramp, and internal splits inside both Washington and Tehran.

The advantage of this method is structured friction. A single narrative can overstate either the diplomatic track or the military track. A multi-agent process forces the Treasury actor to ask how sanctions become leverage, the CENTCOM actor to ask how posture creates accident risk, the Iran pragmatist to ask how talks can happen without humiliation, the IRGC actor to preserve deterrence, and the insurer to price risk before diplomats agree on language.

The simulation does not claim omniscience. It identifies incentive collisions and assigns probabilities to the outcomes those collisions make more or less likely.

Key Findings: US Iran Talks Update

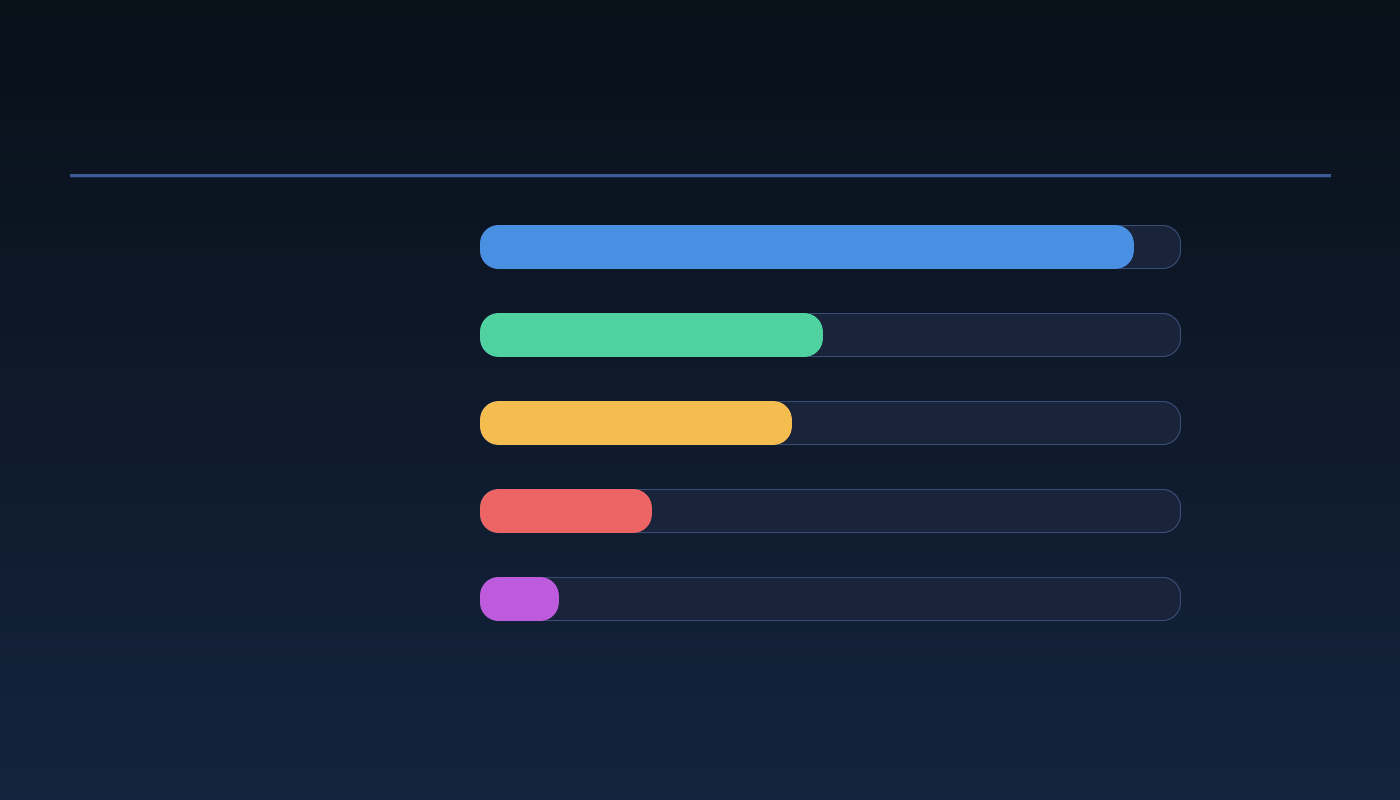

The final probability distribution was:

| Scenario by 2026-05-10 | Probability | Core Mechanism |

|---|---|---|

| Coercive stalemate with intermittent backchannel contact | 42% | Sanctions, threats, naval posture, and quiet messages coexist |

| Pakistan or Oman-mediated talks regain primacy | 24% | A procedural channel resumes and maritime tension cools |

| Wider maritime and trade confrontation | 18% | Shipping, insurance, sanctions, or interdiction triggers a trade shock |

| Short military incident followed by urgent de-escalation | 11% | A tactical clash creates a brief scare, then mediators intervene |

| Surprise mini-deal or pause-for-pause arrangement | 5% | Narrow sequencing around envoy travel, sanctions tempo, or restraint |

Strait of Hormuz pressure is leverage and trap

Iran's useful leverage is also its trap. Hormuz pressure restores deterrence credibility because it reminds Washington, Gulf states, China, shippers, and oil traders that Iran can impose costs outside the nuclear file. But that leverage decays quickly if it causes a visible market shock. A sharp insurance repricing event could unify actors against Tehran, including some actors that otherwise resist U.S. escalation.

That is why the simulation did not produce a high-probability formal closure scenario. Closing or heavily disrupting Hormuz would threaten flows Iran still needs, expose China-linked trade, and invite a harder multinational maritime response. Calibrated ambiguity is more useful than a declared blockade.

Iran oil sanctions become the clean escalation ladder

The U.S. Treasury sanctions architect became one of the most influential agents by the end of the run. Sanctions provide visible pressure without requiring a direct military step. They can target brokers, ship managers, insurers, Chinese intermediaries, shadow fleet logistics, and financial conduits. This gives Washington a way to claim toughness while CENTCOM quietly tries to prevent tactical incidents.

The problem is that sanctions enforcement is not frictionless. The more enforcement focuses on shipping and shadow trade, the more maritime behavior changes. Vessels alter routing, insurance terms tighten, port actors become cautious, and traders price disruption. That means sanctions can remain below the threshold of war while still creating the conditions for a maritime and trade confrontation.

Iran Pakistan talks remain useful but deniable

The simulation found a 24% probability that Pakistan or Oman-mediated talks regain primacy. That is not the base case, but it is large enough to matter. Pakistan remains useful if both sides need a face-saving procedural bridge. Oman remains useful because it is quieter and less politically exposed. The most plausible diplomatic formula is not a grand bargain. It is a narrow exchange of red lines, sequencing, and restraint signals.

Public diplomacy is the hard part. Washington hawks do not want to look like cancelled pressure gave way to talks. Tehran does not want to look like it came back under duress. That makes deniable contact more likely than a visible breakthrough.

Market Implications: Oil, Shipping, and Insurance

The first market implication is an oil risk premium before any confirmed closure. Traders do not wait for a formal announcement when a chokepoint narrative becomes credible. The global oil trader agent repeatedly front-ran ambiguity. In practical terms, that means price action can amplify weak signals, especially if headlines mention vessel warnings, tanker exposure, Gulf port security, or sanctions affecting China-Iran flows.

The second implication is shipping caution. A container line, tanker operator, or charterer does not need certainty to adjust risk protocols. It needs asymmetric downside. If a route becomes marginally more dangerous, managers review insurance, timing, flag exposure, ownership links, and port calls. This commercial caution can then be interpreted by officials as evidence that the adversary is escalating.

The third implication is insurance as an early warning system. War-risk underwriters can transmit geopolitical fear into costs faster than diplomats transmit reassurance. If premiums rise sharply for Gulf or Hormuz transit, that is not just a market reaction. It becomes an input into policy. Hawks use it to argue that pressure is necessary. Mediators use it to argue that time is running out. Iran may read it as proof that its leverage works. All three reactions can occur at once.

The fourth implication is China exposure. Beijing wants discounted Iranian oil and stable routes, but it does not want a sanctions and shipping crisis that makes its trade channels politically radioactive. The China energy planner in the simulation pushed for lower visibility, continuity, and pressure on Iran not to endanger flows. This makes China a dampener of outright escalation, but not a supporter of U.S. enforcement.

Second-Order Effects

If the crisis remains a coercive stalemate, Pakistan and Oman gain relevance without gaining control. They can carry messages, but they cannot force either side to accept a public concession. That creates a durable pattern of private contact and public pressure.

If shipping premiums move sharply, the crisis shifts from diplomatic bargaining to commercial management. Governments then respond to market behavior rather than only to adversary statements. This is the most important second-order effect in the simulation.

If U.S. sanctions increasingly target China-Iran shadow trade, the conflict becomes less about a single negotiation and more about the plumbing of sanctions evasion: ship managers, brokers, transponders, insurance, ports, and payment networks. That expands the number of actors that can accidentally escalate the crisis.

If Israel pushes against an early off-ramp, any public U.S.-Iran channel becomes harder to sell. The simulation did not make Israel the controlling actor, but it did make Israel a friction multiplier inside the pressure coalition.

If Gulf states feel exposed, they will push privately for restraint while avoiding public alignment that makes them look like staging grounds. UAE and Saudi incentives therefore lean toward containment: constrain Iran, keep trade open, and avoid a missile or port-risk panic.

Risk Assessment

The main risk to the simulation is event discontinuity. A single vessel seizure, drone shootdown, missile incident, port strike, or misidentified shadow tanker could move the outcome distribution in hours. The 18% maritime and trade confrontation scenario is not the modal path, but it is the scenario with the highest capacity to change prices quickly.

The second risk is political theater. If Washington or Tehran decides that domestic credibility requires a more visible gesture, the deniable channel could weaken. The model assumes both sides prefer leverage over uncontrolled war. That is structurally sound, but it can be overridden by a leader choosing optics over risk management.

The third risk is data opacity. Shipping, sanctions evasion, and insurance markets often move before public reporting catches up. By the time open sources confirm a routing change or premium move, the decision chain may already have shifted.

The fourth risk is that the Pakistan and Oman tracks are not interchangeable. Pakistan has visibility and relevance, but visibility can become liability. Oman has credibility and discretion, but less public signaling value. If one channel is overexposed or discredited, the other can help, but not perfectly.

Conclusion

The most likely US Iran talks outcome by 2026-05-10 is coercive stalemate, not a clean diplomatic restart and not a deliberate Hormuz crisis. The simulation assigns 42% probability to a tense holding pattern where sanctions, threats, naval posture, insurance caution, and intermittent backchannel contact coexist.

The decisive variable is control over second-order effects. Tehran can use Hormuz ambiguity to restore deterrence, but it risks triggering the very market reaction that turns leverage into isolation. Washington can use sanctions to show pressure, but it risks moving the conflict into shipping and insurance channels that are harder to control than press statements. Pakistan and Oman can keep the door open, but they cannot make public compromise painless.

The practical takeaway is simple: watch the insurers before the diplomats. If war-risk premiums, shipping advisories, and China-Iran trade enforcement stabilize, the stalemate holds and quiet talks remain possible. If those signals spike together, the crisis stops being mainly about envoy travel and becomes a commercial confrontation around the Strait of Hormuz.