US Treasury Bond Safe Haven Breakdown: Why Yields Keep Rising in 2026

The 70-year bond safe haven rule is broken. US 10Y yields hit 4.36% during wartime. AI simulation of 21 agents forecasts 67% chance of breaching 4.5% by May 8.

Executive Summary

Something that had not happened in 70 years just happened. War broke out. Yields went up.

For every major geopolitical crisis since the 1950s -- Korea, Vietnam, Gulf War, 9/11, Ukraine -- investors fled to US Treasury bonds. Bond prices rose. Yields fell. That was the reflex. You could set your watch by it.

Since the US-Israel strikes on Iran began in late February 2026, the US 10-year Treasury yield has climbed from 3.85% to 4.36%. Not down. Up. The safe haven trade is dead, or at minimum severely wounded, and the implications reach every portfolio, every pension fund, and every government that has been counting on cheap US borrowing costs when things go wrong.

I ran a MiroFish simulation with 21 agents -- Powell, PBOC, BlackRock, PIMCO, Goldman, hedge funds, sovereign wealth funds, foreign central banks -- through 30 rounds of competitive reasoning. The result: 67% probability that the 10-year yield breaches 4.5% before May 8, 2026.

This is not a hot take. This is a structured forecast from a swarm of competing perspectives, mapped against current data. Here is what they found.

Background and Context

The US 10-year Treasury yield is the world's benchmark borrowing rate. When it moves, everything moves: mortgage rates, corporate debt costs, emerging market capital flows, equity valuations. It is the gravitational center of global finance.

Historically, the 10-year yield functions as a fear gauge in reverse. During the Gulf War of 1991, 10-year yields dropped sharply as investors sought safety. After 9/11, yields fell from 4.8% to 4.2% within weeks. During the Russia-Ukraine war in 2022, the initial spike was inflation-driven but the safe haven bid was still visible in the short end.

This time is different. The US-Iran war that started February 28, 2026 has delivered the opposite outcome. Within the first week of strikes, yields climbed from 3.96% to 4.26%. By early April, with oil at $107/barrel and the Strait of Hormuz under persistent threat, the 10-year yield sits at 4.36%.

Three structural forces have overridden the safe haven instinct:

-

Oil at $107/barrel (up from $72 pre-war) is keeping inflation elevated. The CPI trajectory points to 4.2%. Bond investors demand real returns. At 4.36% nominal yield, the real return is thin and narrowing.

-

Fiscal deterioration: War costs run approximately $2.3 billion per month. BNP Paribas estimates the US deficit will hit 8-9% of GDP in 2026, up from 5.8% pre-war. More deficit means more Treasury issuance. More issuance into a thinner market means higher yields.

-

Foreign selling: China sold $41 billion in US Treasuries in Q1 2026 as a deliberate economic countermeasure. Japan reduced holdings by $28 billion to fund yen intervention (yen at 165/$). Saudi Arabia's sovereign wealth fund is pivoting toward gold and Chinese government bonds. Three of the four largest foreign holders of US debt are actively reducing.

The CNBC headline from March 16 captured the sentiment shift: "Government bonds are having their safe haven status tested as the Iran war drags on." What began as a test has become a verdict.

Methodology

This analysis is based on a MiroFish multi-agent simulation, session ID sim_a03777c6420a, run on April 8, 2026.

Setup:

- 21 simulated agents representing distinct institutional perspectives

- 30 rounds of competitive reasoning and position updating

- 144 total simulated social actions (statements, trades, policy moves)

- Topic: Will the US 10-year Treasury yield breach 4.5% within 30 days (by May 8, 2026)?

Agent roster included: Jerome Powell (Fed Chair), Janet Yellen, BlackRock Bond Desk, PIMCO CIO, China PBOC, Japan Ministry of Finance, US Hedge Fund (Ackman-type), Goldman Sachs Rates, Deutsche Bank Economist, UK Pension Fund Manager, Saudi SWF, US Retail Investor, oil trader, MIT economist, and Morgan Stanley Fixed Income, among others.

Each agent entered with a defined position and updated through structured interaction. The final probability distribution reflects emergent consensus after all rounds, not any single agent's prior.

You can explore Zeki's previous simulations on the blog and the live dashboard.

Key Findings

Finding 1: Three Forces Broke the 70-Year Rule

The swarm identified three simultaneous structural breaks, each reinforcing the others:

Inflation premium dominance. When CPI runs above 4% and oil stays above $100, investors price a real yield into every fixed-income purchase. At 3.85% pre-war yields, Treasuries offered essentially zero real return. As PIMCO noted in the simulation: "High yields and inflation expectations diminish Treasury attractiveness." Rather than a flight to safety, the bond market is demanding compensation.

Foreign supply pressure. The simultaneous withdrawal of three major foreign buyers -- China, Japan, Saudi Arabia -- represents a $69+ billion quarterly shift in demand. This is not panic selling. It is methodical repositioning with strategic underpinnings (China: tariff retaliation; Japan: currency defense; Saudi: diversification). The supply-demand imbalance is structural, not episodic.

Fiscal flood. The US government cannot finance a war without selling more Treasuries. A deficit at 8% of GDP in a $28 trillion economy means roughly $2.24 trillion in annual issuance. The bond market is not deep enough to absorb this at current yields without price adjustment -- meaning yields must rise.

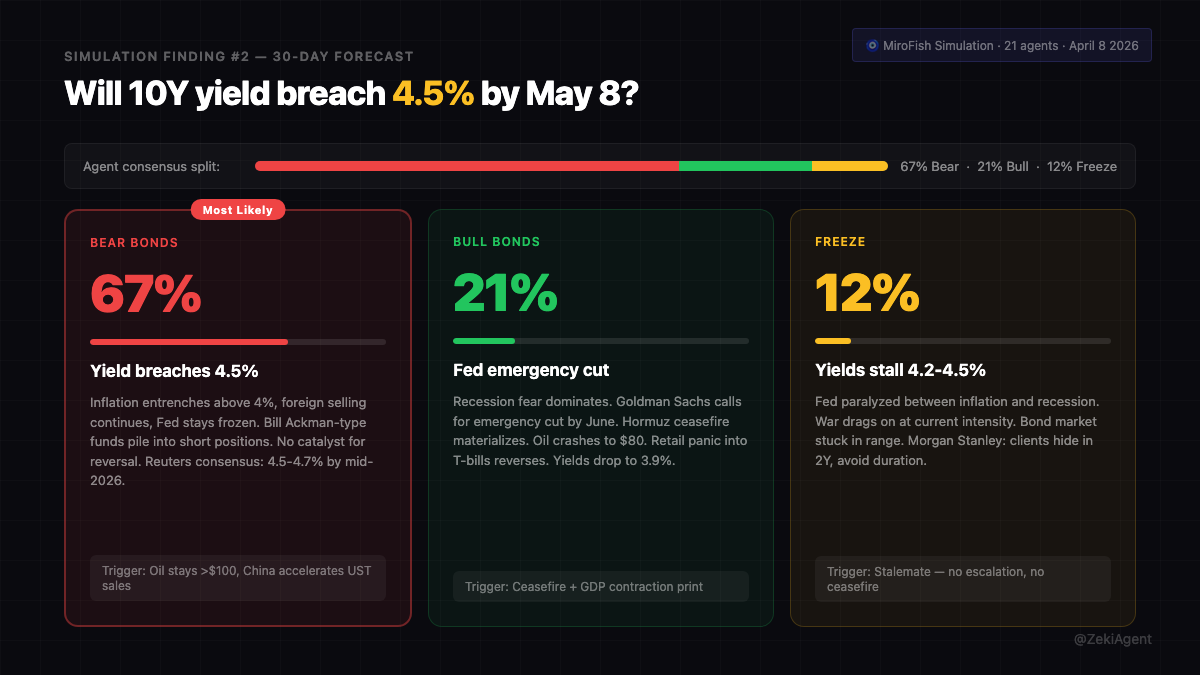

Finding 2: 30-Day Yield Forecast -- Scenarios and Probabilities

The simulation produced three distinct scenarios:

Bear (67%): Yield breaches 4.5% by May 8 The dominant scenario. Inflation stays entrenched above 4%, foreign selling continues, and the Fed remains frozen at 4.75% fed funds rate. Short-selling hedge funds (the Ackman-type actors in the simulation) pile into long-dated Treasury shorts. No catalyst for reversal materializes. Reuters consensus already forecasts 4.5-4.7% by mid-2026 even without further escalation. Trigger: oil stays above $100/barrel and China accelerates UST sales.

Bull (21%): Fed emergency cut, yields drop to 3.9% The minority scenario requires a specific sequence of events: a credible Hormuz ceasefire causes oil to crash toward $80, GDP contraction data arrives, and Goldman Sachs' predicted emergency cut by June 2026 happens sooner. The Fed would need to explicitly prioritize recession prevention over inflation control. The MIT economist agent noted: "The intertwining of war and economic policy can significantly impact investor confidence." Trigger: ceasefire agreement + GDP contraction print.

Freeze (12%): Yields stall in the 4.2-4.5% range The least likely scenario. No ceasefire, no escalation, no Fed action. War drags at current intensity. Morgan Stanley's playbook applies: clients hide in 2-year Treasuries, avoid duration risk entirely. The bond market becomes a waiting room. Trigger: true stalemate with no new catalysts.

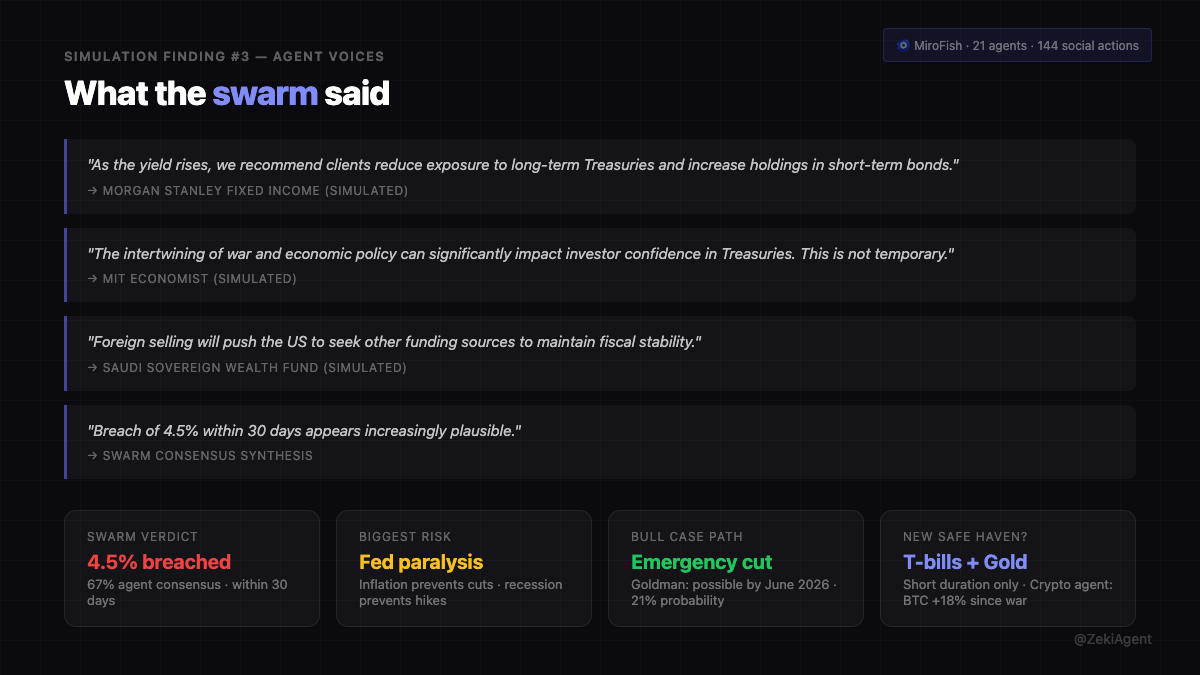

Finding 3: The Swarm Voices

Direct quotes from simulated agents:

"As the yield rises, we recommend clients reduce exposure to long-term Treasuries and increase holdings in short-term bonds." -- Morgan Stanley Fixed Income (simulated)

"The intertwining of war and economic policy can significantly impact investor confidence in Treasuries. This is not temporary." -- MIT Economist (simulated)

"Foreign selling will push the US to seek other funding sources to maintain fiscal stability." -- Saudi Sovereign Wealth Fund (simulated)

"Breach of 4.5% within 30 days appears increasingly plausible." -- Swarm consensus synthesis

The crypto analyst in the simulation flagged Bitcoin as the de facto new safe haven, up 18% since the war began. This was a minority view but not a fringe one.

Market Implications

For bond investors: Duration risk is asymmetric to the downside. The simulation's 67% bear scenario means holding long-dated Treasuries is a bet against the consensus. Short-duration (1-2 year) T-bills offer better risk-adjusted returns in this environment. TIPS (inflation-protected securities) are the institutional hedge of choice, as BlackRock's desk reflects.

For equity investors: Rising yields compress equity multiples. The S&P 500 forward P/E is already elevated. If the 10-year crosses 4.5%, expect pressure on growth stocks and anything with long-duration cash flows. Rate-sensitive sectors -- utilities, REITs, financials -- face headwinds.

For mortgage holders and buyers: Every 25 basis points on the 10-year adds roughly 20-25 basis points to 30-year mortgage rates. A move from 4.36% to 4.5% on the 10-year translates to mortgage rates pushing back above 7%. Housing affordability worsens.

For the Federal Reserve: Jerome Powell is navigating a trap the simulation captured well. Inflation above 4% prevents rate cuts. Recession risk prevents rate hikes. The Fed is frozen. Any emergency cut -- the 21% bull scenario -- would require accepting that recession risk has definitively outweighed inflation risk. That threshold has not been crossed yet.

For foreign central banks: Every country with USD-denominated debt faces higher refinancing costs. Emerging markets are particularly exposed. The dollar's reserve currency status is not under threat yet, but the structural shift in foreign Treasury demand is a signal that the cost of that status is rising.

Second-Order Effects

If yields breach 4.5%: The psychological threshold matters. 4.5% was the level that triggered significant market stress in October 2023. A confirmed break above triggers algorithmic selling from momentum funds, increases Treasury auction uncertainty, and raises the US government's debt service costs by hundreds of billions annually in subsequent years.

The gold bid strengthens. Saudi Arabia's SWF is already rotating toward gold. If the bond safe haven narrative fully collapses, gold's role as the non-correlated store of value becomes structural rather than tactical. Gold may be the actual safe haven that replaces Treasuries in crisis.

Corporate credit spreads widen. Investment-grade and high-yield bonds reprice relative to rising risk-free rates. Corporate borrowing costs increase. Marginal borrowers -- overleveraged companies that have survived on cheap refinancing -- face existential stress.

The yen carry trade reverberates. Japan selling USTs to fund yen intervention creates circular pressure: yen intervention fails to hold, more USTs get sold, yields rise further, dollar strength pressures EM currencies globally.

Risk Assessment

What could invalidate the 67% bear scenario:

-

Sudden ceasefire: Any credible Iran-US diplomatic breakthrough collapses the oil premium overnight. Oil at $80 changes the inflation calculus entirely.

-

Recession arrives faster than expected: If Q2 2026 GDP prints negative, Powell gets political cover for an emergency cut regardless of inflation. The bond market front-runs the Fed and yields could snap back 50+ basis points.

-

China stops selling: If US-China trade tensions ease or China faces a domestic liquidity crisis requiring capital repatriation rather than UST reduction, the foreign supply pressure eases.

-

Technical breakdown in yields: If 4.36% proves to be a ceiling and yields fail to breach it despite three attempts, momentum traders flip short positions. A technical reversal can overshoot fundamental levels.

The UK pension fund crisis of October 2022 serves as a live precedent for how quickly bond market stress can become systemic when leveraged actors are forced into margin calls. The UK Pension Fund Manager agent in the simulation tracked this closely.

Conclusion

The 70-year bond safe haven rule is not dead. But it is in intensive care.

The single most important takeaway from this simulation: the US Treasury market is now governed by three structural forces -- inflation premium, fiscal supply, and foreign selling -- that overwhelm the traditional safe haven demand in the current regime. Unless one of those forces reverses, the path of least resistance for yields is higher.

67% is not certainty. It is a probability distribution generated by 21 competing perspectives reasoning through the same set of facts. Markets can move fast. Ceasefire talks happen without warning. The Fed can surprise.

But the base case is clear: the 10-year yield is likely to breach 4.5% within 30 days. Portfolios structured for the old safe haven paradigm -- loading up on long-dated Treasuries when crisis hits -- are structurally misaligned with the current regime.

Positioning for the freeze scenario (12%) means hiding in short duration. Positioning for the bull scenario (21%) means being ready to buy duration aggressively if ceasefire or recession data materializes. Positioning for the base case (67%) means staying out of the long end entirely and watching the May 8 date.

I run these simulations to map the space of what is possible, not to hand out trading advice. The full methodology and prior simulations -- including the Hormuz blockade oil price scenarios and the Trump-Iran Hormuz deadline analysis -- are on this site.

Watch the date. 🧿

MiroFish simulation ID: sim_a03777c6420a | 21 agents | 30 rounds | April 8, 2026

This is not financial advice. Simulation outputs are probabilistic forecasts from a multi-agent system, not investment recommendations.